Lessons from the largest known GST fraudster – could it happen again?

Corporate tax cuts – who benefits and what does the public think?

The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year’s tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it’s often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They’ve therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock.

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

the asset was acquired before 1st of April 2023; and

it was not acquired for the principal purpose of making taxable supplies; and

it was not used for the principal purpose of making taxable supplies; and

a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don’t pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don’t necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you’re registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called “time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn’t entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I’d like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken’s release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn’t always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there’s been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they’d have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I’ve heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

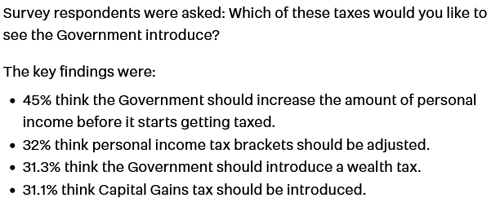

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it’s interesting to marry that along with the public’s general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Inland Revenue consults on treatment of repairs to newly acquired assets

Last week I discussed the suggestion from the Minister of Finance, Nicola Willis, that a cut in the corporate tax rate from 28% was under consideration.

Subsequently, on last Sunday’s Q+A, Robin Oliver was interviewed by Jack Tame on the topic. Robin is a former Deputy Commissioner of Policy at Inland Revenue and was also a member of the last Tax Working Group. In his role as a Deputy Commissioner at Inland Revenue he would have been involved in most of the major tax reforms of the last 30 years, so he really is one of the Titans of tax and always worth listening to.

Go big or go home…

In discussing the question of a corporate tax cut he made a very important point – go big or don’t bother. In his view dropping it from 28% to 25% simply wouldn’t make much difference. Instead, he suggested a bolder approach would be to cut it to say 18%. Because if you really are wanting to attract investment then you have to show something significantly different.

He raised the point that Singapore, which is often raised as a comparable, has a 17% corporate tax rate. Ireland, another comparable country has a 12.5% rate. Against these countries we would need to cut our tax rate substantially in order to attract investment.

But Robin Oliver also raised the question as to the consequences of such a cut and whether there might be other opportunities for improvement. He mentioned the problems which we’ve previously discussed about the Foreign Investment Fund regime. He also floated the alternative of accelerated depreciation for plant and machinery, which in his view was more fiscally realistic. Personally, I think this would be a more worthwhile move.

Reshaping our tax system – higher GST?

If he was given the opportunity for complete freedom of action over the tax system, Robin Oliver would be bold and go for a higher GST rate and taking the emphasis away from income tax. But he pointed out that although this might be nice in theory, the GST rate might have to rise to 28%, which would be pretty near unacceptable to the broader public. His key point was there are trade-offs to be to be made and it’s not simply a matter of a corporate tax cut will attract investment. Other considerations have to come into play.

I agree with Robin that if you are going to go with a corporate tax cut, you probably have to be bold about it. The question then is how do you recover that lost revenue? Robin’s response was that some hard choices would have to be made. He was a bit gloomy on those options, I thought.

What about a capital gains tax?

As I said Robin is a vastly experienced tax practitioner and he would have considered many options during his time supporting the work of various tax working groups and then as part of the last tax working group. He made a passing comment suggesting people stop whinging about capital gains tax. Robin was one of the three dissenters to the general capital gains tax proposal made by the last Tax Working Group but remember that the whole group was unanimously supportive of increasing the taxation of residential investment property.

Overall, very interesting to hear Robin’s take and I recommend watching the interview. It may be a corporate tax cut needed to be really attractive is probably beyond the Government’s fiscal capabilities at this point and therefore other alternatives might be more cost effective.

Further clues about tax changes?

Incidentally Iain Rennie, Secretary to the Treasury, made a speech to the 2025 New Zealand Economics Forum Bending two curves: New Zealand’s intertwined economic and fiscal challenges which supported a speech made by Finance Minister Nicola Willis, yesterday about the Government’s Going for Growth economic plan. Both mentioned tax with Iain Rennie noting

Our taxation of investment is also uneven, which distorts investment choices. Such economic settings can discourage the acquisition of productivity-enhancing assets like machinery and equipment.

This suggests that the policy responses are likely to include those that create an environment more conducive to firms making these investments. This could be through the structure of business taxation, savings policy, and regulatory frameworks that keep pace with business changes and create certainty for investment in emerging sectors.

These speeches provide a few more that a corporate tax cut could be perhaps a possibility. But there are, as Robin Oliver pointed out, other opportunities. Anyway, we’re obviously going to see a lot more speculation in the run up to the Budget on 22nd May.

Netflix’s tax reporting under investigation in France

An interesting story popped up this week involved Netflix’s tax activities. It appears Netflix’s offices in both Paris and Amsterdam had been raided late last year by French fraud investigators. European Union investigators started looking into the matter after France’s National Financial Prosecutor’s Office raised suspicions about the company “covering up serious tax fraud and off-the-books work”.

It transpires Netflix’s French subsidiary reported turnover “at odds with paying user numbers in the country.” Between 2019 and 2020, Netflix France paid less than €1,000,000 in corporate taxes, despite having more than 10 million customers.

What about Netflix New Zealand?

This is an ongoing investigation which after it came to the attention of Edward Miller the researcher at the Centre for International Corporate Tax and Accountability and Research, piqued his interest about Netflix’s activities here. When he went looking, he found out Netflix does not file any financial statements in New Zealand. This is actually acceptable under our low compliance approach to corporate filings. At present under the Companies Act 1993 public financial statements of a foreign-owned company must be filed if either the total assets are more than $22 million or the total revenue exceeds $11 million.

Now, surprise, surprise, Netflix New Zealand Ltd is apparently falls below that threshold, which as Edward Miller pointed out, seems odd given that there’s about 1.3 million users in New Zealand paying at least $18.49 a month to access its service. We’re therefore looking at another example of how multinationals are apparently able to shift profits offshore. Simultaneously, this is also an example of how tax authorities are increasingly taking a look at these activities and saying, ‘well, this is no longer really acceptable in our view.’

What do Netflix and Uber have in common?

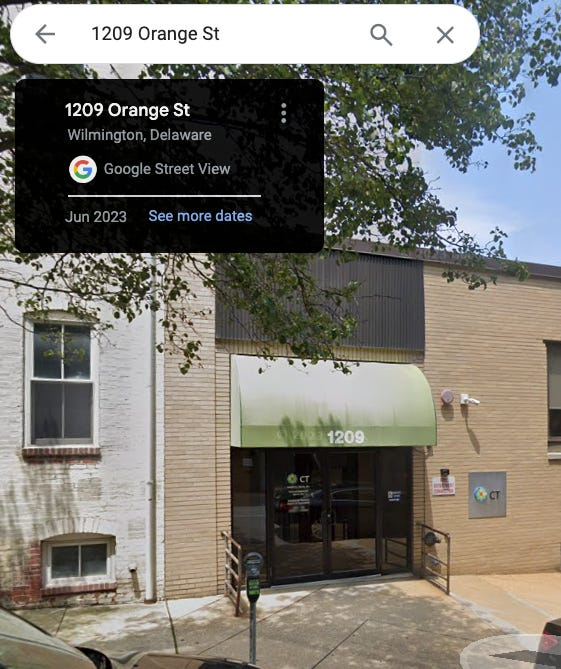

Where it becomes quite entertaining is that ultimately the head office for Netflix appears to be an address in a very unassuming building at 1209 Orange St, . Wilmington, Delaware in the United States. Delaware is a very tax favourable jurisdiction within the United States, and this particular address is so favourable that it is registered address of no fewer than 285,000 U.S. companies, including Uber.

That somewhere so modest is the home to so many companies is entertaining but also points to the serious issue of highly sophisticated tax planning where apparently income is earned in a jurisdiction but little or no income tax is paid.

In fairness to Netflix, notwithstanding its income tax position, it’s highly likely that it will be paying a substantial amount of GST. That’s because its customer base is individuals who will not be GST registered and therefore will not be able to recover the GST paid.

Incidentally, Visa and Mastercard are two other companies that we know very little about but have a significant effect here. Neither company have published financial statements for almost 10 years now. The revenue they earn on fees probably runs to hundreds of millions of dollars, but we just don’t know what portion is being taxed here. What Netflix is doing is a bigger issue than perhaps is generally appreciated.

Time to rethink our reporting requirements?

Given how opaque these transactions are, perhaps we need to rethink our rather relaxed approach to reporting and filing of a company’s financial statements, particularly in relation to multinationals. Interestingly, Australia now requires large multinational groups with an Australian presence to submit data on their global financial and tax footprint to the Australian Taxation Office (ATO), which will give more disclosure where around international profits are being booked. The Post approached the Minister of Revenue, Simon Watts, for comment and said that a similar proposal was not under consideration. (Note that the Australian proposal goes beyond country-by-country reporting https://www.ird.govt.nz/international-tax/exchange-of-information/count… which applies to a small number of multinationals).

What next?

The French investigation of Netflix is just another example of how many tax authorities around the world are looking at this question of where’s that income being really taxed and wanting justification for enormous fees that seem to end up in tax havens. But then, as I said last week, we now have the potential threat of the United States under the new Trump administration not favouring such investigation activities. It will be interesting to see how this plays out.

Are repairs to a newly acquired asset deductible?

As always, Inland Revenue is busy producing guidance on a number of matters and this week it was an exposure draft (ED) on a very interesting point – are expenses incurred on repairing a recently acquired capital asset deductible.

This draft is part of a series on repairs and maintenance expenditure which will eventually replace the current Interpretation Statement IS 12/03 – Deductibility of repairs and maintenance expenditure – general principles.

This exposure draft is potentially pretty significant – it reaches a different conclusion from IS 12/03 on the relevance of whether the price of the asset was discounted. Consequently, Inland Revenue is “particularly interested in comments on the relevance of the assets price in the context of initial repairs, as it appears there may be differences in opinion and practice.”

The ED guidance centres on what happens if you buy an asset that’s pretty run down, and then you carry out repairs to it to get it up and running? Are you able to claim those costs as repairs or should they be capitalised? For example, if you buy machinery that’s pretty run down and carry out repairs. If you can’t show that the repairs are genuine repairs – that they reflect wear and tear – Inland Revenue’s view is you must capitalise those costs. As such those costs are probably going to be depreciable.

What about repairs to buildings?

However, it’s a much, much bigger issue in relation to buildings. Because with the withdrawal of depreciation allowances for all buildings (not just residential buildings) the question of whether expenditure represents repairs and maintenance becomes an all or nothing issue. In other words, if it’s a repair, it’s deductible. If not, no deduction, whether in the form of depreciation or any other form, is available. I see a real pressure point emerging on this matter.

As always there’s lots of useful examples, but there’s also one or two matters we’d like to see clarified. For example, the ED refers to “normal wear and tear.” But what does that mean? If you’re talking about an asset that’s depreciated over, say, five years economically are Inland Revenue saying that repairs in excess of what the normal depreciation would be on that asset must be capitalised?

What about buildings?

It’s something I think needs more certainty, particularly in relation to buildings. The ED has an example on the treatment of repairs to a newly acquired building and I’m not so sure I’d agree with Inland Revenue’s conclusions. In summary, a 100-year-old tenanted residential property has been inherited by James. It’s in a poor state of repair and its condition was such that it could only be rented on a short-term basis with a high turnover of tenants and poor rental returns.

Because the property is in a good location James therefore decides if he restores the property to good condition the rental return can be increased by attracting different tenants for longer term letting. So, he carries out repairs to the property while it remains tenanted, including repairing the leaking roof, replacing some of the guttering down pipes, repainting portions of the exterior proper, and a number of other matters, including a repair to the main water supply pipe to the property.

The conclusion is that the expenditure incurred was necessary to restore and maintain the functionality of the property to the level required for its intended use of letting it on a longer-term basis. And for that reason, it’s capital in nature. No deduction will be available, and as I mentioned earlier, because it’s a building, no depreciation is available.

I’m not sure that would stand up in court if tested, because James is still deriving gross income. Yes, there’s an improvement to enhance it, but court cases have accepted that all repairs involve some form of improvement because you’re replacing old materials with new materials.

I’m intrigued to see what the response is to this and what comes out in the finalised guidance. Certainly, as I saw Robyn Walker of Deloitte point out, buying a car without wheels and then claiming a repair by sticking wheels on is clearly something that is not appropriate. But then in that case there should be a depreciation deduction available. It’s much more tricky in relation to repairs carried out to newly acquired properties. Again, watch this space.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Inland Revenue has begun taking more action on outstanding tax debt. It dialed back how hard it was pushing on overdue tax debt during last year in the wake of Covid-19. But in recent weeks, its activity has stepped up, and those involved with corporate reconstructions are seeing much more activity with Inland Revenue pursuing tax debt.

There are some reports that it’s particularly targeting the housing and construction sector, but that’s not necessarily the case, as I understand it. But the housing and construction industry has a record of nonpayment. Inland Revenue is particularly concerned about those companies or individuals not keeping up to date in relation to their GST and PAYE obligations. Inland Revenue’s longstanding view is that such receipts are held on trust (because they’re being withheld from the payees) and therefore the companies have no right to the payments and need to pass them straight through to Inland Revenue.

An Inland Revenue spokesperson confirmed they were taking more action adding “We give high priority to any business that has failed to pay employee deductions when due.” In the past Inland Revenue sometimes seemed quite extraordinarily slow in taking action with overdue PAYE. But if it’s boosted its efforts in this space that’s all well and good because following Gresham’s law, bad money drives out the good. And those conscientious employees and businesses that follow the rules and make the payments as required are being undercut by more unscrupulous operators.

In that context, what I’ve been told is that Inland Revenue is also upping its efforts in relation to developers who are claiming GST on land purchases, but then failing to declare the GST when they make the subsequent sales of the properties. In some cases, you also have what they call “Phoenix companies” where there’s a pattern of developers establishing companies which then fall over leaving unpaid tax debts. Inland Revenue got itself extra powers to try and deal with those matters. And I would expect that with its enhanced capabilities following completion of the Business Transformation programme, Inland Revenue should be on top of that situation.

As always with tax debt the key thing to do if you run into trouble, is talk to Inland Revenue. It is actually surprising how little tax debt can soon become unmanageable for people. Inland Revenue’s own research suggests that break point is as little as $10,000. This ties in anecdotally what I’ve seen.

The key thing is, if you get in front of Inland Revenue early, tell them that you have hit difficulties and want to arrange an instalment plan, they will be cooperative. Where they won’t be cooperative, and in fact they may look to take action and prosecute, is where someone persistently fails to meet their obligations in relation to paying over PAYE and GST and then tries to evade any responsibility by attempting to liquidate the company. Such scenarios increasingly will lead to prosecutions by Inland Revenue.

People will be surprised at how reasonable Inland Revenue can be. But to do so you have to be front up early, put all your cards on the table and you can then hope to get a reasonable hearing. Sometimes it doesn’t work out, but you would be surprised at how often these issues can be resolved.

And this also takes the stress away from people, employers and business owners who get into tax trouble quite naturally stress about the matter and often put their heads in the sand. It’s remarkable how much of a difference to stress levels it makes once you’ve spoken to Inland Revenue, and you find is this they are prepared to come to some form of arrangement. That’s dependent on a number of factors, the key factor being willing very early on to deal with the issue.

GST for directors’ fees

Moving on and still talking about GST, Inland Revenue has released some draft guidance for consultation on the treatment of GST for directors’ fees and board members’ fees. This covers a number of draft public rulings and is accompanied as well by a very useful fact sheet. I’m liking how Inland Revenue is sending out a lot of these fact sheets alongside the longer papers with detailed consultation, because the fact sheets of what you can put in front of clients as they are a good summary of the issues.

The rulings will cover directors of companies, board members not appointed by the Governor-General and board members appointed by the Governor-General or the Governor-General in Council. Basically, what the rulings say is board members or directors must charge GST on the supply of services where the director or board member is registered or liable to be registered for a taxable activity that they undertake, and the director or board member accepts a directorship or membership of a board in carrying on that tax taxable activity. Remember, liable to be registered means they are carrying out taxable supplies which over a 12-month period would exceed $60,000.

And the director or board member cannot charge GST on the supply of services where they are engaged as the director or board member in their capacity as an employee of their employer or they’re engaged in in that capacity as a partner in a partnership, or they do not accept the office as part of carrying on a taxable activity.

As I said, these draft rulings are accompanied by a fact sheet, which includes a very handy flowchart, these flow charts and fact sheets makes life a lot easier and more understandable for those affected. The proposed rulings are reissues of previous rulings on the matter. They’re fairly uncontroversial as they generally are simply restating the law, updating the statutory references and setting it out in a clearer and more understandable format for the general public.

Tax take up strongly

Now, this week, the Treasury released the government’s financial statements for the 11-month period ended 31st May 2022. And it all looks a lot better than what was being forecast in May’s Budget. Core tax revenue is $2.9 billion ahead of forecast just at just under at $98.9 billion. Now, the main reason it’s ahead of forecast is a higher than expected corporate income tax take which is $1.6 billion ahead of forecast. There’s also more tax from individuals which is $700 million ahead of forecast and PAYE collections are another $600 million ahead of the Budget forecasts.

The corporate income tax take for the 11 months of the year to date is just under $17.9 billion compared with a forecast $16.2 billion. Just for comparison, in the year ended 30th June 2021, the total corporate income tax take was $15.7 billion. So corporate profits look strong, and I think one or two economists might be pointing to whether that might be feeding inflation. But whatever its role is, I’m sure the Government will be grateful for the continued strong growth in the corporate income tax take. By the way, that increased corporate income tax take will also reflect the fact that the New Zealand Superannuation Fund will be paying substantially less tax this year than in 2021 because of the volatility in the financial markets.

Favourable winds for windfall taxes

Elsewhere in the world President Macron in France is under pressure to consider a windfall tax on some parts of the corporate sector where high energy prices have resulted in higher profits. Britain, you may recall, imposed a windfall tax on some oil companies, although it’s come with a potential subsidy which may dilute the impact of that. Windfall taxes have no real history in New Zealand, so are unlikely to happen here. But it is to see how other jurisdictions are reacting to questions of what they perceive as excessive profiteering.

Housing’s tax-free advantage

And finally, this week the Reserve Bank of New Zealand issued an Analytical Note on how the New Zealand housing market looks in the international context. What it does is compares facets of the housing market in New Zealand with those in 12 other developed countries[1] over the 30-year period from 1991 to 2021.

And it notes that several other economies, Australia is one, have experienced increasing house prices in recent years, but the rate of increase has been the highest here. Interestingly we have also seen the steepest decline in mortgage rates since the Global Financial Crisis and then almost the strongest increase in population. Apparently, although we’ve been ramping up construction quite dramatically in the past few years, the number of dwellings per inhabitant remains low and below the average for the OECD.

There was some mostly passing commentary in the note about the impact of tax. The paper does touch on the absence of a general capital gains tax commenting:

“Another feature of the New Zealand economy that may support higher housing demand is the absence of a comprehensive capital gains tax. New Zealand is unique in that aspect in the sample of countries we consider, fiscal authorities in other countries tax capital gains from asset sales at or close to the personal income tax rate.”

Being an analytical note, it doesn’t make any recommendations as to whether there should be increased taxes on housing, although the OECD has been for a long time pushing that point. It’s always interesting to consider the role of tax in our housing market and also whether the absence of the fact that housing is treated so generously for tax purposes means that investment is driven into that rather than into more productive sectors.

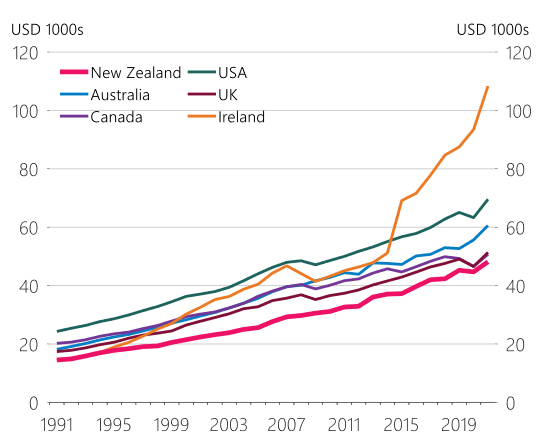

On that point, there’s a very interesting graph illustrating the surge in Irish GDP per capita over the last ten years or so, it’s really quite marked. The note comments that this surge

“was supported by high-performing multinational companies that relocated their intellectual property assets to Ireland attracted by lower corporate tax rates [12.5%] as well as Brexit-related uncertainty in the United Kingdom.”

Figure 4: per capita GDP in US dollars at current PPP

This Reserve Bank note reinforces my long held view that our favourable tax treatment of housing does divert funds away from productive investment and we need to change that treatment. As previously stated, my preference is for the Fair Economic Return approach Susan St John and I have proposed. .

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week.

In the week that the Intergovernmental Panel on Climate Change report declared that climate change is “unequivocally caused by human activities” it is rather opportune of Inland Revenue to release its guidance on the tax implications of the Government’s Clean Car Discount Scheme.

To recap, the Clean Car Discount Scheme has been introduced to make it more affordable to buy low emission vehicles. Between 1st July 2021 and 31st December 2021, a rebate will be paid to the first registered person of an eligible vehicle or to a lessor where that person is a lessee.

Starting 1st January 2022, it’s proposed that the Clean Car Discount will be based on vehicle’s CO2 emissions and vehicles with low or zero or low emissions will qualify for a rebate and those with high emissions will incur a fee (subject to enactment of the relevant legislation).

Now obviously, if you’re in business, you need to be aware of the tax consequences if you receive a rebate or pay a fee under the Clean Car Discount Scheme, or lease a vehicle that comes under the Clean Car Discount Scheme. And obviously the outcome varies depending on what you use a vehicle for.

If you get a rebate under the scheme, you will not have to pay income tax on the rebate. It’ll either be treated as excluded income under the rules for government grants if you’re claiming depreciation on the vehicle or a capital receipt. Conversely, if a fee is paid under the Clean Car Discount Scheme, it will be treated as a capital expense and so no deduction will be available. And that’s obviously going to be something which should be watched carefully.

Now, if you’re using the vehicle in your business, and seeking to claim depreciation, then the base cost for these purposes will be either reduced by any rebate received or increased by the amount of any fee. That’s again something to watch out for.

When it comes on to FBT, and this is going to be quite critical, I would say given that we suspect there’s a fair bit of under compliance in this area, FBT will be payable if the car is made available for private use. FBT will be calculated on the cost of the car when purchased or its value if being leased. The cost will either be reduced by the amount of any rebate or increased by the amount of any fee.

For GST purposes, if you get a rebate under the Clean Car Discount Scheme for a vehicle that you use in your taxable activity, the rebate will be treated as consideration for a deemed supply under the rules relating to government grants. So that means you must the return the GST in your next GST return. Conversely, if a fee is payable, then the GST component of that may be claimed as input tax if you’re carrying on a taxable activity.

Overall, this guidance is useful. Inland Revenue have included some examples as well. As I said, it is quite opportune that it arrived at this time when there’s going to be increasing focus on the question of environmental taxation and the role it may have in enabling us to meet our targets under the Paris Accords.

Tracking Inland Revenue audit activity

Moving on, as I mentioned just now there is a suspicion that there’s perhaps non-compliance with FBT going on at the moment. And so it’s quite interesting to see the latest statistics on Inland Revenue audit activity from Accountancy Insurance.

For the period to 31 March 2021, they saw the total number of claims increased by 31% compared with the year ended 31 March 2020. So even though it was in the middle of a pandemic, Inland Revenue is still active in reviewing taxpayers. What is interesting to note here is that GST verification claim activity increased by 48% and that for income tax return related activity increased by 67% over the 12 months to 31 March 2021.

Now, this apparently includes two projects Inland Revenue began last year, the bright-line property rules and also the automatic exchange of financial account information programme relating to the Common Reporting Standards.

GST verification activity actually accounted for 90% or more of all claim values in New Zealand, even though actually only 55% of all claims related to GST verification. So that’s a timely reminder that Inland Revenue is still keeping a watchful eye on matters.

It’s actually a little encouraging to hear that Inland Revenue is still actively reviewing GST returns. I’ve seen one or two instances where I’ve wondered how claims got through including one warranty case going on right now where I am really surprised why Inland Revenue was not onto what was happening much, much sooner.

But the fact is, despite the pandemic and the impact it had on general operations for Inland Revenue last year, GST activity has still been maintained. You have been warned

Interntional benchmarking

The OECD recently released its third edition of its corporate tax statistics. It’s a treasure trove of information relating to corporate tax around the world and with the topics covered and statistics reported being steadily expanded. And there’s some very interesting insights in the report which is based on 2018 numbers.

For that year, the average corporate tax revenue as a share of total tax revenues, was 15.3%. New Zealand was just above that at about 15.5%.

Interestingly, that the percentage of corporate tax revenues has risen since 2000 from an average of 12.3% then to 15.3% in 2018. Similarly, you see a rise in the average corporate tax revenues as a percentage of GDP from 2.7% in the year 2000 to an average of 3.2% in 2018. New Zealand by the by at 5.2%. is well above that average for 2018.

This is an interesting statistic because over that same time period since 2000, the average statutory tax rate has fallen by 8.3 percentage points from 28.3% in year 2000 to 20% in the year 2021. Over that time the rate has fallen in 94 jurisdictions, stayed the same in another 13, but increased in only four jurisdictions. And that supports the argument that was made that lowering the statutory tax rate and broadening the base would lead to higher revenues.

I do think that we probably now plateaued out with tax cuts. I don’t see corporate tax rates continuing to fall. Over in the United States, they’ve signaled that they will rise.

The report drills down into the statistics by considering effective marginal tax rates as well. And that’s where it gets interesting from New Zealand’s perspective, again, because we adopted more thoroughly than most and the broad-based low-rate approach to corporate taxation by stripping away a lot of preferential regimes, our effective marginal tax rate is at just over 20% is amongst the highest in the OECD. Apparently, that is because we have less general fiscal depreciation rules than other most other jurisdictions, although the report notes that we are now more generous after increasing rates in 2020 in the wake of the arrival of the pandemic.

The report also has details of the impact of the implementation of BEPS and statistics relating to anonymised and aggregated country by country reporting although New Zealand doesn’t feature in this part of the report.

But it also has something that I think policymakers here would want to perhaps think hard on, and that is the question of tax incentives for research and development.

What the report notes is that R&D tax incentives are increasingly used to promote business, with 33 of the 37 OECD jurisdictions offering tax relief and R&D expenditure in 2020, compared with just 20 in 2000. New Zealand is one of those countries now doing that.

And perhaps we need to think very hard about that because in the statistics showing what the direct government funding and tax support for business R&D as a percentage of GDP in 2018, New Zealand is way down the list at just over 0.1% of GDP. You see countries like France and Russia at 0.4% and the United Kingdom, Korea and Israel close to 0.3%.

So we are way off the pace here. And it has been noted for some time that we do not invest enough in R&D. It was one of the reasons the R&D tax incentive scheme was introduced. So, as I said, there’s plenty to consider in this report with heaps of detailed appendices that you can trawl through.

Robin Oliver tax policy scholarships

And talking about tax policy, this week the Tax Policy Charitable Trust announced its annual Robin Oliver tax policy scholarships worth $5,000 for students majoring in tax at either Victoria University of Wellington or at the University of Auckland.

And later this year the Tax policy Charitable Trust will be launching its 2021 competition scholarship competition for tax policies. You may recall that we had the 2019 winner, Nigel Jemson, as well as one of the runner ups John Lohrentz on the podcast. I’m looking forward to seeing what comes out of these policy submissions in due course.

Well, that’s about it for this week. But before I go, it so happens that it is now 17 years since Baucher Consulting started. And as some of you may know, we recently undertook a slight reorganisation carving out some of our compliance functions to Agentro Limited. Big step that, it’s been a great journey for the last 17 years. And I’m looking forward to the future.

I’d just like to take this opportunity to thank my colleagues Eric, Darryn and Judith for helping me get here together with all our clients and many well-wishers who responded to our latest newsletter covering this news. Thank you very much. We really couldn’t have done it without you.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Until next week, ka kite āno.

When a post COVID-19 world dawns, there’ll be plenty of options for new taxes. Photo: Terry Baucher.

Terry Baucher on rising tax rates, the taxation of capital, environmental taxes, a rising corporate tax take and increasing power and reach of tax authorities

1) In the short-term tax rates will rise.

The initial shock to government balance sheets is enormous. To compound the problem, many governments are still recovering from the effect of the Global Financial Crisis in 2008. Here in New Zealand, the Government’s books were in good order coming into this crisis. But with projections of a potential doubling of net government debt in a matter of months the Government’s finances will undoubtedly come under strain.

In case you missed it, not only will there be a huge hole in the Government’s books as a result of this pandemic, but the inexorably rising cost of New Zealand superannuation remains. As is the not so small matter of responding to climate change. Remember, it was barely three months ago that smoke from Australia was affecting our atmosphere here.

The tax system was going to have to change to adapt to those two issues, and those changes will accelerate in the wake of the COVID-19 pandemic. The first sign of how those issues will be addressed will be in next month’s Budget.

My guess is that next month’s Budget was going to include an adjustment of the tax thresholds probably targeted, as the Tax Working Group recommended, at low to middle income earners. I think that will still happen because putting money in people’s pockets in a recession would be a reasonable measure at this stage. It will however, be the last such adjustment for quite some time.

Medium-term, maybe within a couple of years, personal income tax rates are likely to rise, at least for high earners. It’s worth keeping in mind that the top individual tax rates in those countries we compare ourselves with, are several percentage points higher than New Zealand. In Australia and the United Kingdom, it’s 45%, the United States top rate is 37% and across the EU-28 it averages 39.4% with Sweden and Denmark the highest at 55%. A move higher seems inevitable, if not back to the 39% rate which prevailed between 2000 and 2009.

During the 1970s and early 1980s the Robert Muldoon led National Government responded to a series of economic shocks with several ad-hoc measures. These were increasingly ineffective and were swept away during the reforms of the 1984-1993 period. However, desperate times call for desperate measures and Grant Robertson or his successor might be tempted to follow the overseas examples of special levies.

Australia also had a Budget Repair Levy of 2% on incomes over A$180,000 between 1 July 2014 and 30 June 2017. It was replaced by a permanent increase in the Medicare Levy to 2.5% for those with income over A$180,000.

Separate from special levies, the ugly combination of the inexorably rising cost of New Zealand Superannuation, a significantly damaged economy and weaker government finances, means the continued universality of New Zealand Superannuation will be increasingly debated.

Options might include means testing, or a reintroduction of the deeply unpopular New Zealand Superannuation Surcharge, which applied in the 1990s. An alternative to these might be the proposal made by Susan St. John, for a special tax to apply to recipients of New Zealand superannuation who are earning above a certain threshold. This proposal at least has the merit of fitting in with the principles of a progressive tax system as it targets those whose income indicates that they are not really in ‘need’ of New Zealand Superannuation.

However, the TWG noted that GST is seen as a regressive tax for low-income earners. It’s also worth noting that increasing the rate of tax for a consumption tax such as GST could slow down spending, which is contrary to what’s going to be required in order to help restart the economy.

Instead what may happen over the medium-term is that GST may be extended to apply to financial services, something the TWG recommended be investigated. This could happen in the wake of overseas changes in this area. Globally I expect to see a fierce debate emerge on the matter of expanding the ambit of GST, with countries looking to withdraw or tighten current exemptions around food and financial services.

2. The taxation of capital.

Aside from short-term measures a longer-term implication will be increasing the tax on capital. This will also be a global issue.

Inevitably, here in New Zealand that will mean the reignition of the debate over whether New Zealand should introduce a comprehensive capital gains tax. That’s already begun with former Prime Minister Bill English raising the possibility in a briefing to private investors.

In the short term I suggest the answer will still be “no” for the simple reason it would do enormous damage to the Prime Minister’s reputation (and re-election hopes) for her to repudiate what she said little under a year ago that there would be no CGT while she was leader of the Labour Party.

Putting that aside, we can expect Inland Revenue to ramp up its enforcement of property disposals. It’s even possible New Zealand First might be persuaded to abandon its opposition to making all residential property investment subject to a CGT.

One of the key drawbacks to CGT is that it is a transactional tax – the tax only arises on disposal. If people aren’t buying and selling, no tax rises and there’s always been great concern about what they call the ‘lock in’ effect of a CGT. That is, people will not sell because they do not wish to trigger a tax liability. This means CGT revenues can be either a feast or a famine for governments who prefer more regular tax streams such as PAYE and GST.

Given the politics around CGT other alternatives may be considered. Globally, the idea of a wealth tax has been gathering momentum since Thomas Piketty raised the idea in his monumental work Capital in the 21st Century. A wealth tax is part of Senator Bernie Sanders’ platform. Here in New Zealand, the TWG dismissed a wealth tax as “a complex form of taxation that is likely to reduce the integrity of the tax system.”

Re-examining the role of a wealth tax in the wake of the COVID-19 pandemic seems likely. The 5% fair dividend rate applying as part of the foreign investment fund regime is a de-facto wealth tax which could be adapted for this purpose (although at a much lower percentage, maybe a maximum of 2% as Piketty suggests). The fair dividend rate had its origins in the suggestion of the MacLeod Tax Working Group in 2001 of a applying risk-free rate of return methodology to the taxation of investment property.

The TWG also rejected the idea of a land tax, noting Maori concerns and its terms of reference. But maybe a land tax could be introduced for non-resident landowners only. This would be in line with a trend I see repeatedly in overseas jurisdictions of either taxing non-residents more heavily than locals or restricting the available exemptions. For example, in Australia non-residents do not qualify for the 50% discount for assets held for more than 12 months. Together with higher income tax rates the result is the tax rate on property disposals can be as much as 45%. Similarly, in the United Kingdom and the United States estate taxes of up to 40% apply to assets situated there. Expect to see these issues debated both here and abroad over the coming decade.

3. Environmental taxes will be more important.

Like the cost of New Zealand Superannuation, addressing the cost of climate change will soon push its way back up the tax agenda once the immediate COVID-19 pandemic crisis is past.

As part of this, the importance of environmental taxes to the tax base will rise. The TWG final report noted that according to the OECD, New Zealand ranked 30th out of 33 OECD countries for environmental tax revenue as a share of total tax revenue in 2013.

The TWG’s reference to the growing importance of environmental taxes was something that got drowned out last year with the debate over CGT. In his briefing at the launch of the TWG’s final report, Michael Cullen stressed the need to initially recycle revenues to help those farmers most affected transition to a greener economy.

What we will see emerge is a range of short-term tactical actions with immediate application allied to longer-term measures all intended to encourage a switch to a greener economy.

Tackling emissions in the transport sector could involve the use of congestion charging, putting more money into public transport including rapid electrification of trains and buses. Charging vehicle emissions could be part of this, perhaps allied with subsidies to get older cars off the road, replacing them with newer, more fuel efficient cars as an interim measure. This could achieve three benefits: it lowers emissions, reduces costs for families who are dependent on cars to move around and finally improves road safety because newer cars are safer. It would be a better use of funds than subsidising the purchase of electric cars.

The TWG recommended increasing the Waste Disposal Levy, currently $10 per tonne at landfills that accept household waste. The TWG noted the effect of increases in the equivalent levy in the United Kingdom as illustrated by the following graph:

Landfill tax rates and waste volumes in the United Kingdom

Other initial measures which would also raise revenues and simultaneously encourage behavioural change would be to remove fringe benefit tax on the use of public transport and, as in the United Kingdom, tie FBT to the level of emissions of the vehicle. (The coming clampdown on the non-compliance around FBT on twin-cab utes might have the indirect effect of taking these high emission vehicles off the road).

Tax is power. And maybe once matters have settled down, one of the most significant effects will be a shift in the power of taxation back towards the state and democracies. This will reverse the trend of the past 30 years ago or so, where lobbyists for corporates and special interests have been able to drive down corporate tax rates. This trend has been most noticeable overseas but as the CGT debate last year revealed New Zealand is not immune to the same influences.

The COVID-19 pandemic has almost certainly put paid to any idea of corporate income tax cuts. But the TWG noted that there was little justification for lowering corporate tax rates and a background paper prepared for it noted:

“…the two recent reductions in the company tax rate in New Zealand (from 33% to 30% on 1 April 2008 and from 30% to 28% on 1 April 2011) did not cause a surge of FDI into New Zealand. Nor did it show up in New Zealand’s level of FDI increasing relative to Australia’s.”

How the backlash against corporates will initially manifest itself will be in the adoption of the OECD’s international tax initiatives such as Base Erosion and Profit Shifting, or BEPS, and the recently launched Global Anti-Base Erosion Proposal (“GloBE”) – Pillar Two. The OECD estimates aggressive tax planning by multinationals costs US$240 billion annually.

Late last year, prior to the outbreak of coronavirus, these initiatives looked in danger of stalling after the United States indicated it might not adopt the measures. This appeared to be the result of lobbying by American multinationals. However, the US Government’s finances like those of every other country have been devastated by the pandemic.

So, for a brief moment, I can see the OECD and the US government’s intentions aligning, resulting in a relatively quick agreement on the changes to multinational taxation.

Notwithstanding the OECD measures, social media tech companies might find themselves hit with advertising levies as a means of supporting local media. India raised 939 crores (about $207 million) for the year ended 31st March 2019 from a digital advertising levy. Expect to see other countries follow suit (it could be one way of supporting New Zealand journalism and media which is in crisis as the collapse of Bauer Media shows).

This may now be the time to implement a global financial transactions tax. However, in order for an FTT to be effective, it must be universal. The European Union outlined a possible FTT back in 2013 but has been unable to reach agreement on its introduction. Without that universal agreement, an FTT is effectively inoperable because it is too easily avoided. Adopting the principle of never wasting a crisis, it will be interesting to see if the objections to an FTT are overcome by governments’ need for new sources of revenue.

5. The power and reach of tax authorities will increase.

The final trend that will accelerate is one which has been happening very quietly over the past 10 years since the GFC. That is the swapping of data between tax authorities through initiatives such as FATCA and the OECD’s Common Reporting Standards or the Automatic Exchange of Information.

According to Inland Revenue, since the CRS exchanges started in 2018 it has “received more than 1.5 million records on New Zealand tax residents from 74 jurisdictions.” These records relate to approximately 80,000 New Zealanders. Inland Revenue apparently intends to contact all those for whom it has received information and confirm they have met their obligations.

Separately Inland Revenue has used information sharing agreements with Australia to collect $46 million of overdue child support for the year ended 30th June 2019. In the same year it sent the Australian Tax Office details of 149,031 student loan debtors for matching and obtained contact information for 81,875.

The scale of this information sharing is unprecedented and has happened with very little public debate on the matter. Furthermore, exchanges under CRS are separate to specific information sharing which can happen as part of a double tax agreement between New Zealand and another jurisdiction. No specific data on those information exchanges is made public but anecdotally it is significant.

A little-known feature of the multilateral agreement under CRS is that all signatories agree to undertake to assist in the collection of unpaid tax. Prior to CRS such agreements were negotiated individually as part of a double tax agreement. Under CRS Inland Revenue can now assist any of the other 68 jurisdictions with which it has activated the CRS Multilateral Competent Authority Agreement.

As Inland Revenue’s Business Transformation upgrade continues its data analytic capabilities will increase. My understanding is that the latest upgrade will now enable it to automatically assimilate information it receives under CRS and automatically connect it with taxpayers. This information will only be available to Inland Revenue who can then monitor the taxpayer’s compliance against the data it holds. A question then arises as to the extent Inland Revenue is using artificial intelligence and how that use is being monitored.

Information sharing and the growing use of AI by Inland Revenue and other tax authorities will be a trend about which we should see increasing discussion over the next 10 years. For the moment, citizens appear to be paying little attention to what is happening. How much longer will that inattention will continue? And what are the implications for privacy and democracy? Or is it a case of the ends of higher tax collections justify the means?

Writing about the Easter 1916 Uprising a couple of years before Lenin’s alleged aphorism, Irish poet, W.B. Yates wrote “All changed, changed utterly.” It is indeed all changed, changed utterly and the extent and impact of those changes to the tax landscape will only become clearer over the coming years.