The OECD proposes a crypto-asset reporting framework

New levy proposal for farmers’ greenhouse gas emissions;

TOP’s bright idea about tax rate

Last week, the OECD launched its Crypto-Asset Reporting Framework (CARF). This is a response to a G20 request that the OECD develop a framework for the automatic exchange of information between countries on crypto-assets. In other words, it is going to be a development of the existing Common Reporting Standards on the Automatic Exchange of Information or CRS. The CARF was presented to G20 Finance Ministers and Central Bank Governors for discussion at their meeting this week in Washington D.C.

The proposed rules cover four areas:

the scope of crypto-assets to be covered,

the entities and individuals subject to data collection and reporting requirements,

the transactions subject to reporting as well as the information to be reported in respect of such transactions and

the due diligence procedures to identify crypto-asset users and controlling persons and to determine the relevant tax jurisdictions for reporting and exchange purposes.

CARF is intended to complement the CRS and mean that crypto-assets will be subject to automatic exchange of information reporting. Now the reason that that has come up is unsurprising really. Individuals holding wallets which are not affiliated with any current financial institution or service provider, and are therefore then able to transfer crypto-assets across jurisdictions. As the OECD report notes:

“this presents the risk that relevant crypto-assets are used for illicit activities or to evade tax obligations. Overall, the characteristics of the crypto asset sector have reduced tax administrations visibility on tax relevant activities carried out within the sector, increasing the difficulty of verifying whether associated tax liabilities are appropriately reported and assessed”

This is a very long way of saying there’s probably a lot of tax evasion going on in the crypto-assets sector.

CARF is therefore an obvious response. It is also part of the huge ongoing trends in the modern tax world of the acceleration in reporting and exchange of information between jurisdictions. This is a very, very significant development in the tax world that happened in the wake of the Global Financial Crisis and has largely gone unreported in the wider press although it appears to be generally accepted by the public. When you align this alongside what’s happening with the Pillar One and Pillar Two proposals, then the days of tax havens where money can be parked outside the tax net of major jurisdictions, are numbered.

So what crypto assets are covered? Well, the definition is pretty broad, it targets assets “that can be held and transferred in a decentralised manner and without the intervention of traditional financial intermediaries”, i.e. banks and other financial institutions. This includes stablecoins, derivatives issued in the form of crypto-assets and certain nonfungible tokens.

There are three categories excluded from what’s termed “Relevant Crypto-Assets”:

crypto assets, where have it’s been determined they cannot be used for payment or investment purposes,

Central Bank Digital Currencies which represent a claim in Fiat Currency on an issuing Central Bank or monetary authority, which function similar to money held in a traditional bank account,

Specified Electronic Money Products that represent a single Fiat Currency and are redeemable at any time in the same Fiat Currency. (Not sure I’ve encountered any of these myself, to be honest).

Reporting entities are any intermediary or service provider which is facilitating exchanges between relevant crypto-assets or between relevant crypto-assets and fiat currencies. Generally, they will be subject to the reporting requirements of the jurisdictions in which they are either tax resident or have a regular place of business or branch through which they carry out reportable transactions.

Keep in mind, CARF ties in with the CRS which is already hugely comprehensive and covers most of the main tax jurisdictions and tax havens. The ability for crypto asset service providers to slip out from underneath the CARF reporting requirements is going to be quite limited.

Three types of transactions are going to be reportable:

exchanges between Relevant Crypto-Assets and fiat currencies,

exchanges between one or more forms of Relevant Crypto-Assets, and

transfers of Relevant Crypto-Assets.

CARF has been developed to sit alongside CRS and in fact at the same time the OECD carried out its first comprehensive review of the CRS regime. It’s proposing some amendments to bring new financial assets, products and intermediates within the scope of CRS. The changes are also being made to try and avoid duplicate reporting with that which is expected to happen under CARF.

The entire CARF framework runs to over 100 pages. It should be signed off subject to any further work requested by the Central Bank Governors and Finance Ministers at their meeting this week. There will no doubt be some further tweaking, so it’s not yet all set to go. No doubt there will also be some lobbying for changes in the regime.

CARF is, as I said earlier, part of a growing trend for international cooperation on the sharing of information. When implemented it basically will probably mark an end, or certainly a restriction, on the use of crypto assets for tax evasion and other nefarious purposes.

Making farms pay

On Tuesday, the Government released its proposals for how to price agricultural emissions.

These are in response to the recommendations earlier this year from He Weka Eke Noa, the Primary Sector Climate Action Partnership, for a farm level pricing system. The Climate Change Commission, He Pou a Rangi, also provided separate advice on agricultural emissions.

The Government’s proposals try and integrate what He Weka Eke Noa and He Pou a Rangi have suggested. The intention is to price agricultural emissions at the farm level. But it comes with a big stick – if the sector cannot reach agreement by 1st January 2025, then agricultural emissions will be be priced under the Emissions Trading Scheme.

The key part of the proposal is a farm level split gas levy to price agricultural gas emissions. It will apply to farmers and growers who are GST registered and meet certain livestock and fertiliser use thresholds. There would be separate levy prices set for long lived gases and biogenic methane and these will be set up after advice from the He Pou a Rangi and in consultation with the agricultural sector and iwi and Māori.

The long-lived gases (basically carbon) price will be set annually and then linked to the New Zealand Emissions Trading Scheme unit price. There’s a separate biogenic methane levy which will be adjusted based on progress towards domestic methane targets. One of the feedback matters the Government is seeking is whether that methane levy price should be reviewed annually or every three years.

With regards to the revenue raised, the Government proposes it that the revenue is used to fund incentives and sequestration payments, with any remaining revenue to fund the administration of the pricing scheme and a joint government and Māori revenue recycling strategy. There’s a proposal for incentive payments for a range of on-farm emissions reduction technologies and practises. I fully endorse this policy of using funding from an environmental tax to help the transition.

But if you’ve been watching this, you’ll know it has taken a long time to get here. It’s almost 20 years since the infamous ‘Fart tax’ was first proposed and Shane Ardern MP drove a tractor up the steps of Parliament. So progress has been very slow on this, which I personally find very frustrating.

Here in the city, we need to be working on reducing our transport emissions. Rather ironically, on the same day of the Government announcement, Ruapehu Alpine Lifts went into voluntary administration. The ski field operation has clearly been affected not just by one very bad year and the effect of Covid. This is something that’s been building for some time.

We’ve also had the recent floods and damage reports coming out of Nelson where the insurance claims so far total $50 million. So change is happening all around us and my view is we are going to have to adjust to it and try and do something to reduce emissions as part of the global effort. We can’t rely on everyone else to do it for us.

TOP tackles tax bands

Finally, this week, there’s been a lot of talk about tax cuts ahead of next year’s General Election, particularly in the wake of the massive u-turn by the UK government over a proposed higher rate tax cut which has now resulted in the sacking of the Chancellor of the Exchequer (Finance Minister) Kwasi Kwarteng.

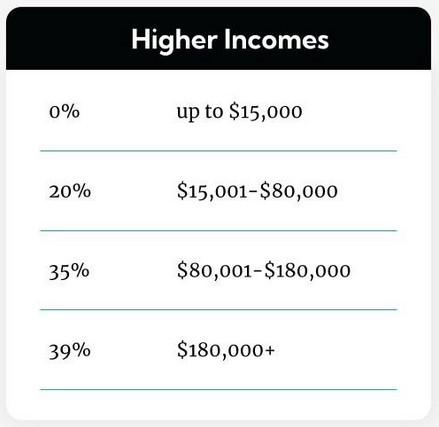

Amidst all of that chaos The Opportunities Party released its two-phase tax policy, phase one of which contains substantial tax cuts. But what caught my eye about TOP’s suggestion is their proposal to introduce a tax-free threshold of $15,000, together with adjusted tax thresholds.

Now tax-free thresholds are expensive, but they are seen around the world. Australia has one for the first A$18,200. The UK tax free personal allowance is £12,570 and America has a flat $12,000 exemption.

But what I thought is interesting about TOP’s proposal is they have looked at the question I’ve talked at length about what happens for low- and middle-income earners when their income crosses the current $48,000 threshold and the rate jumps from 17% to 30%. Under our current tax structure 12.5 percentage point jump is the highest such rate – the next jump at $70,000 is only from 30% to 33%.

So, I’ve been thinking for some time that we really ought to be looking at these thresholds and rate bands and maybe combining three into two, which is what TOP propose.

Now, TOP have got to either win an electorate or get across the 5% threshold before they’ll be in any position to propose their policy. (The second part of their policy would fund those tax cuts by a land value tax, which, of course, is longstanding TOP policy). We’ll have to wait and see until after next year’s election.

But if you want to hear more about what type of tax changes could happen and their implications then this week on RNZ’s The Detail podcast, Jenée Tibshraeny of the Herald and I spoke to Sharon Brettkelly about tax cuts here and in the UK, how our tax system works and what could be done if we’re helping people at the lower income level.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

The Taxation Annual Rates for 2021 to 2022 GST and Remedial Matters Bill was introduced to Parliament on Wednesday. Now this is the annual bill which is required to confirm the tax rates for the current year. And it also contains a number of GST and income tax remedial amendments. It doesn’t, by the way, include anything in relation to the proposed interest limitation rules. Those are going to be introduced separately, probably later this month, by way of a Supplementary Order Paper.

Now, what’s particularly interesting about this bill is that it clarifies the tax treatment of cryptoassets, and it has two proposed amendments which would exclude cryptoassets from GST and the financial arrangements rules.

As the commentary to the bill points out, cryptoassets probably fall within the existing scope of GST rules, although it’s a little unclear. And that means that the supply of a cryptoasset could be subject to 15% GST, or it could be an exempt financial service or a zero-rated supply to a non-resident. And what this means is that GST supply to a non-resident is zero rated, but then subject to GST when applied to residents. And that creates a distortion and a preference to sell to offshore investors. Now, that’s slightly different from the zero rating we do for exports, but it’s not seen as an export service here.

But more importantly – and this is an issue that’s well known – is that there’s a big risk of potential double taxation. That is when an asset is purchased with Bitcoin and then, for example, that Bitcoins converted back into fiat currency.

The commentary gives an example of Lucy purchasing $11,500 of Bitcoin from a domestic Bitcoin exchange. At present, the exchange is required to remit $1,500 dollars of this, being GST, to Inland Revenue on the taxable supply of Bitcoin they’ve made in exchange for New Zealand dollars. When Lucy uses the $11,500 of Bitcoin to purchase a car, GST applies on the sale of the car and therefore the company selling the vehicle must return another $1500 dollars of GST. So that means that GST of $3,000 has effectively been charged in relation to the purchase of a vehicle worth $10,000. If Lucy had used New Zealand dollars instead of Bitcoin, only $1500 of GST would have been paid.

This has been known for some time and what has happened is that the Government has decided they’re going to take cryptoassets out of the GST net. And the proposal is that the definitions of goods and services in the Goods and Services Tax Act will be amended to expressly exclude cryptoassets. Now, this amendment will apply from 1st January 2009, the date of the first cryptoasset, Bitcoin, was launched. By the way, the definition will exclude non fungible tokens, which are going to remain subject to GST if supplied by a registered person.

So this is a very welcome development, clarifying the position that was causing some concern in the cryptoassets world, for the reasons and the example I gave a bit earlier – that there was a probable chance of GST being charged twice in essence, on the same asset. But just remember that GST is still intended to apply for non-fungible tokens as they’re regarded as a good or service that can be supplied.

Now, the other big amendment, which will be welcomed by investors in the cryptoassets world is that cryptoassets will be excluded from the financial arrangements rules. That will be done by amending Section EW5 of the Income Tax Act 2007 to define cryptoassets as an accepted financial arrangement.

Again, however, the issuing of non-fungible tokens are not financial arrangements and they do not meet the definition of a financial arrangements set up in the Section EW 3 of the Income Tax Act. This proposed amendment will also apply from 1st January 2009.

But there is one exception that people need to be aware of, that is cryptoassets will not be treated as an accepted financial arrangement if the owner receives amounts that are determined by reference to the purchase price of cryptoassets, and on the basis that is known by the owner in advance. The purpose of this exclusion is to say that cryptoassets that are economically equivalent to debt arrangements are still taxed under the financial arrangements rules.

And the commentary has an example of such a treatment. An investor invests in Bitcoin on a platform and Bitcoin is locked in for a set period and the investor is paid a guaranteed fixed return for the period that his Bitcoin remains locked into this particular platform. The commentary makes clear that the return on the growth will be taxable, so the additional 5% return will be subject to the financial arrangements rules. I think there might be some more questions dealing around that.

And the commentary also makes clear that the general rules still apply to cryptoassets. That if they’re acquired with the purpose of disposal, they’ll be taxable. Likewise, if you’re trading cryptoassets or you use cryptoassets for a profit-making scheme. But as I said, all the proposals will be welcomed by the investors in the cryptoassets world.

Now, the bill also has proposed amendments in relation to the bright-line test. Firstly, any income derived on the sale of a property which has been used as a main home will not be reduced where the person has used the main home exclusion twice in a two-year period or has engaged in a regular pattern of acquiring and disposal disposing of residential land.

The bill also has an amendment to ensure that a main home that takes longer than 12 months to construct will not be subject to the bright-line test. And this is in relation to residential land acquired on or after 27 March 2021. There’s also an amendment to clarify the application of the 12-month buffer and makes clear that a person may still qualify for the main home exclusion if they have multiple periods each of 12 months where the property is not used as a main home. So, again, that’s welcome because there was some confusion around how these rules might apply.

Business subsidies for wide public health impacts

Now, moving on, the Government’s Wage Subsidies bill has passed $1.2 billion dollars so far. And apparently this subsidy is supporting over 838,000 employees, 117,000 self-employed people and 242,000 businesses.

The highest number of supported workers are in the construction industry, followed then by food and hospitality.

Now, it’s also been made clear that although most of the country has stepped down to Level Two – the wage subsidy is not normally available below Level Three – a claim is still possible if part of the country is still in Levels Three and Four. Because Auckland has remained at Level Four, that means that businesses outside Auckland may still apply for the wage subsidy. However, they have to show the 40% drop in revenue required to meet the wage subsidy requirements is attributable to the effect of the continuation of Alert Levels Three and Four.

So that’s a wee caveat in there that people just need to be mindful of. I know that there’s lobbying going on in relation to the hospitality industry, where the impact of Level Two restrictions limit numbers in bars and restaurants to 50 or fewer. Those lobbying want the ability to still apply for a wage subsidy because they’re affected by that Level Two condition, not necessarily because of the ongoing Level Four lockdown in Auckland.

More taxes to pay for an ageing demographic?

And finally this week, government departments have been asked to prepare a series of long term insights briefings under the Public Service Act 2020. Now these are designed to make available to the general public information about medium- and long-term trends, risks, opportunities that may affect New Zealand.

Treasury has also got a requirement to produce a statement regularly on the long-term fiscal position – what’s known as Long Term Fiscal Statement, and what it’s decided to do is combine the two and it’s released a draft paper for consultation, which makes fascinating reading.

One of the things it says, is that looking at the impact of Covid, it thinks net debt will now peak at 48% of GDP in 2023. And in the Treasury’s view, there is currently no need to reduce debt levels. And it believes that deficits will shrink as the temporary support measures will end. And it also notes that debt level remains low relative to its peers such as the UK, Australia, America. The interest rate composition of debt is much more favourable than when net debt peaked at 55% of GDP in 1992.

And just as an aside, this is a global issue. The UK just this week has announced proposals which effectively increase taxes to pay for the impact of Covid and they’re quite significant increases. And I don’t think that the UK will be the last jurisdiction to be doing so.

But longer term, Treasury is noting that 26% of the population is expected to be 65 years old or more by 2060, compared with 16% in 2020. So that’s going to increase the cost of New Zealand superannuation and also expect healthcare costs to continue to grow because of an ageing population. And that ageing population will change demographics. For example, one of the things that’s happening is that the Pasifika/Māori people are generally significantly younger than other New Zealanders.

For example, by 2038, Māori are projected to account for 20% of the total population, but only 10%of the 65 plus population.

And this leads Treasury to conclude:

“Our projections indicate that the gap between expenditure and revenue will grow significantly as a result of demographic change and historical trends in the absence of any offsetting action by the Government.”

One of the offsetting actions it suggests, is to raise the age of retirement from 65. It suggests let’s have a look at what would be the impact of raising it to 67.

It also looks at what opportunities exist to raise revenue from either existing tax basis or new tax bases beyond personal income tax. And the paper sets out a number of options around raising revenue. And one is ten years of fiscal drag, which incidentally we’ve just done, which is where the tax thresholds and rates are not changed. And wage growth naturally raises the tax take as people’s income crosses income tax thresholds.

Some interesting stats here about the impact of raising GST. For example, in relation to personal income tax – if you raise income tax rates by one percentage point, so that the current top rate of 39% goes to 40%, the 33% rate to 34% and so on, that would raise 0.6% of GDP.

To get the same effect from GST you’d need GST to rise from 15% to 16.5%. And for company income tax, you’d need to raise it from 28% to 34%. So as the paper points out that would not be welcome.

The Treasury paper also points out the Government could extend the taxation of capital gains and maybe think about a land tax as well. However, as the Tax Working Group pointed out there’s a few issues around a land tax. But the paper notes, by the way, that other countries are looking at the taxing of wealth, either by a net wealth tax or maybe taxes on inheritance.

And finally, the paper notes that New Zealand raises less from environmental taxes than other OECD countries. It’s equivalent to 1.3% of GDP, and that’s lower than the OECD average, which is roughly 2% of GDP. But it points out that environmental taxes are often behavioural taxes. In other words, they change behaviours but therefore may not be a sustainable additional source of revenue.

Anyway, there’s a lot of interesting data to consider in this paper. No doubt it will cause some controversy.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and colleagues. Until next time Kia Kaha! Stay strong.

A couple of weeks ago, I reported that the Inland Revenue main office in Wellington had been closed and the staff were working from home as a result of a potential earthquake risk which had been identified.

There’s still no timeline as to when Inland Revenue staff, almost over a thousand of them, will be able to return to the office. In the meantime, they’re working from home. And the question has now popped up “Well, how about a bit of reimbursement for extra costs like heating and broadband?”

Now, apparently, Inland Revenue response has been “You’re saving money by working from home. You don’t have to pay for commuting, lunches and all the rest”. But the Public Sector Association is saying, “They have to work from home through no fault of their own.” And maybe it’s time that Inland Revenue recognised that and reimbursed them for it.

One Inland Revenue staff member has noted the argument that he was saving money on commuting costs doesn’t wash, because as he put it, “the five dollars a day I spend travelling in and out of work has never been deemed by Inland Revenue as a work-related expense. It’s a personal expense and it’s not claimable.”

Now, what this points to is a grey area which requires a mix of better tax policy which lays out some better guidelines and perhaps employers as well coming to the party. The position is, as I set out last year, when this whole thing became very, very relevant when we were all working from home during the first lockdown, is that employees cannot claim a deduction for home office expenses. They are meant to be reimbursed reasonable costs by their employer. This apparently seems not to be happening generally and it seems Inland Revenue is also reluctant to do this.

There was a determination issued during last year which covered the pandemic, which said that an employer could pay an allowance to an employee working from home that covers general expenditure and up to $15 per week would represent as exempt income. But $15 a week is pretty low with broadband costs and heating costs.

So the question was raised back then and it’s now back on the agenda again in a slightly more ironical context that we perhaps need to be setting out better guidelines. It occurs to me, for example, in the film industry, I understand per diems have been agreed of around $50 per day for contractors working in the film industry. And that’s taken to be a reasonable estimate of the costs they would have incurred.

The position I’m coming to here is Inland Revenue perhaps needs to grasp the nettle and issue more determinations which are more generous in scope and make it clear that for employers who pay these allowances, the extra allowances will be deductible, and the expenses will be non-assessable for employees.

Working from home does shift some of the costs to the employee. And I think it’s only fair that they get reasonably reimbursed. The legislation is in place, but I think it seems clear that the correct practise isn’t always understood and followed by employers. So maybe setting out new actual monetary limits would be a better approach going forward, even if Inland Revenue seems rather reluctant to do that.

Everyone is looking at cryptoasset taxes

Moving on there is increasing scrutiny of the cryptoasset world, and it’s tied into tax authorities wanting to get a better understanding of people’s assets, plus suspicion that people are using virtual assets to evade tax and also that cryptoassets are part of illegal activities and money laundering.

So as part of that, earlier this week, the United Kingdom Treasury announced a proposal that will require any virtual asset transfer of above £1,000 to be accompanied by detailed personal information of both the originator and the beneficiary.

This is tied into proposed amendments to money laundering legislation required to keep the UK’s regime in compliance with the recommendations of the Global Financial Action Task Force. The Financial Action Task Force said in July 2019 anti-money laundering legislation should cover cryptoassets. Putting the legislation in place has always taken a little bit of time.

Anyway, this is another sign of the increasing attention that tax authorities and authorities generally are paying to virtual cryptoassets.

Over in the United States the Internal Revenue Service, in conjunction with the New York State U.S. attorney’s office, has been briefing experts on the latest U.S. government enforcement efforts related to virtual currencies and cryptoassets.

As of April 2021, the IRS has joined its civil and criminal cryptocurrency units through Operation Hidden Treasure. Its Fraud Enforcement Office and Criminal Investigation Units are working with international law enforcement and crypto industry experts to root out tax evasion. And apparently, these include something called John Doe summonses, which sounds pretty sinister, and no doubt will pop up on some American TV show in due course and be explained to us.

The US Federal tax returns, Form 1040, now includes a question on virtual currency income, and it’s actually at the top of the form. That’s deliberately designed in order to make it easier to prove the knowledge and willfulness element for criminal cases in this matter.

So what we’re seeing is a trend all around the world of really amping up the scrutiny of cryptoassets. It’s a fast-moving field and the tax treatment isn’t always as clear as it could be. But Inland Revenue here is continually issuing guidance on the matter. And people need to pay attention to this. You should expect that the tax authorities will have some idea of your cryptoassets holdings and therefore you should follow the law and file returns as appropriate.

Facing up to unintended consequences

And finally this week, a couple of things in relation to the ongoing arguments over the Government’s interest limitation rules. Firstly, Inland Revenue has issued a very useful precis of all the questions and answers relating to the interest limitation rules and bright-line tests.

At 22 pages it’s a much more digestible document than the main discussion document. And of course, Inland Revenue is still working through all the submissions. So it’s a useful one stop shop to go through and get an idea of what’s been said so far. However, you should not take what’s in this Q&A as actual policy. They’re still working through it and the final version still has to be signed off by the Minister of Revenue and Cabinet.

But meantime, Norman Gemmell, who is the chair in public finance at Wellington School of Business and Government, Victoria University of Wellington, and former chief economist at New Zealand Treasury has come out with a working paper entitled What is Happening to Tax Policy in New Zealand and is it Sensible?

It’s a very quick read about 14 pages which looks at the increase in the top income tax rate and the housing package, that is the interest limitation rules, increased bright-line period and other related matters. Basically, it takes the view that both represent ad hoc responses without a coherent strategy. It notes that these were pushed through very quickly based on limited analysis and against most official advice on the matter as to how to deliver on the Government’s objectives.

And in Gemmell’s view, there are potentially serious unintended consequences. In particular, the coherence of the tax system is at risk, and it’s not an unreasonable argument. In fact, someone quipped that’s a statement of fact not an argument,

But this comes back to what I said last week, that when you look at where there is incoherence in the tax system, it keeps coming back to the question of the taxation of capital and of property in particular. We keep fencing around this issue and the unintended consequences of doing so, force further unintended consequences of the actions taken to try and remedy that.

There won’t be an easy answer to this solution until that nettle is very firmly grasped and the politicians put the politics aside and look at how exactly are we going to achieve a coherent tax system and address the issues of diversion of resources away from productive assets, inequality, and housing affordability.

All of those require a comprehensive approach and taking a different approach to what we’ve been doing up to now. The latest patches may work, perhaps, but they come with unintended consequences as Mr Gemmell points out.

That’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week ka kite āno!

Earlier this week, Parliament’s Finance and Expenditure Select Committee announced it was launching an enquiry into “the current and future nature impact and risks of cryptocurrencies.”

This is a very broad ranging enquiry, the terms of reference include enquiring into and establishing the nature and benefits of cryptocurrency, how they are created and traded, understanding the environmental impact of mining cryptocurrency (which is something increasingly in the news). Identify risks to users and traders of cryptocurrency, what risks cryptocurrencies pose to the monetary system and financial stability. The tax implications in New Zealand and how cryptocurrencies are used by criminal organisations. And to establish whether the means exist to regulate cryptocurrency either by sovereign states, central banks or multilateral cooperation.

Now this is part of a worldwide trend. Cryptoassets are now worth over a trillion dollars following a huge surge in value. Increasingly, governments around the world are looking at what’s going on in this space, particularly as cryptocurrencies are also linked to the ransomware attacks that we’ve been seeing, the most notable example in New Zealand being the Waikato DHB.

Over in Australia, the Australian Tax Office (the ATO) is concerned that many taxpayers are not meeting their obligations, thinking cryptocurrency gains are tax free or only taxable when the holdings are cashed back into Australian dollars. ATO data shows a dramatic increase in trading since the beginning of 2020. It now estimates there are over 600,000 taxpayers in Australia that have invested in cryptoassets.

The ATO has said that it is going to write to around 100,000 taxpayers with cryptoassets, explain their tax obligations and urge them to review their previously lodged returns. That’s quite a big project. It also expects to “prompt” almost 300,000 taxpayers as they lodge their June 2021 tax returns to report their cryptocurrency capital gains or losses. So the ATO has come out swinging.

Over here Inland Revenue has been consistently expanding the release of information on how it considers cryptoassets should be treated. And a couple of weeks back, it released its final versions of a couple of “Questions we’ve been asked” about the consequences of receiving cryptoassets from either a hard fork or an airdrop. These are QB 21/06 and QB 21/07.

QB 21/06 deals with the tax treatment of cryptoassets received from an airdrop. Briefly, it’s saying that receipt of such airdropped cryptoassets are taxable where the person has a cryptoassets business, acquired the cryptoassets as part of a profit-making undertaking or scheme, provided services to receive that airdrop and the cryptoassets are a payment for those services or receives air drops on a regular basis. But beyond these circumstances the airdrop is probably not taxable.

Now, just quickly, an airdrop is basically a distribution of tokens without compensation. What I understand, is that these are undertaken with the view of increasing awareness of a new token. It might also be done to increase the supply of cryptoassets in the market. The income tax treatment will very much depend on the nature and purpose and intent of the investor who receives them.

What happens when a person who received airdropped cryptoassets disposes of them? Well, it’s taxable if it’s part of a business or they provided services to receive them, or they acquired them with the purpose of disposing of them. But in some cases, the cryptoassets were possibly acquired by the investor who was just sitting on a particular cryptoasset and received an airdrop without providing any services for it. So that may not be taxable because can you say that the airdropped cryptoassets were acquired with a purpose of disposal?

QB 21/07 deals with the consequences of receiving cryptoassets from a hard fork. A hard fork, by the way, is generally defined as where the protocol code of the block chain has been changed to create a new version of the block chain outside the old version. You have a new token which operates under the rules of an amended protocol, whereas the original token continues to operate under the existing protocol. An example would be the July 2017 hard fork of Bitcoin which saw the creation of Bitcoin cash alongside Bitcoin.

In the wonderful terminology of the crypto world there’s also a software which updates the protocol but is intended to be adopted by all users on the network. And so no new coin is expected to be created. The example given here is the August 2017 SegWit fork to the Bitcoin protocol.

2017 is probably a century ago in the cryptoassets world as this is a space that’s moving very, very quickly. Hence why the Finance and Expenditure Committee wants to have a look at enquiry into what’s going on.

Now, generally speaking the principles are similar to that of QB 21/06. So, if someone’s received cryptoassets following a hard fork, it’s taxable if they’re in a cryptoassets business or acquired the cryptoassets as part of a profit-making scheme or undertaking. In most other circumstances, the receipt is not taxable.

However, when cryptoassets received from a hard fork are disposed of, those will be taxable again, where the person has a cryptoassets business or acquired the cryptoassets as part of a profit-making undertaking a scheme or for the purpose of disposing of them.

As ever, there’s a lot going on in the cryptoassets space. Inland Revenue is, like most other tax authorities, and the ATO is a good example, trying to keep up with the play here. It will be interesting just to see how matters develop. Australia has a capital gains tax, so to borrow a line from Blondie “One way or another, they’re going to get you”. But here the rules are a little less clear. It’s actually good Inland Revenue is setting out rules, but the pace of change means that it’s probably sometime behind the eight ball.

GST on meal expenses for the self employed

Moving on, Inland Revenue released an Interpretation Statement IS 21/06 last week. This deals with the income tax and GST treatment of meal expenses incurred by self-employed persons.

Now, this is quite a substantial document, it actually runs to 37 pages, because what it also does is discuss the treatment of meal allowances paid to employees. It does so to illustrate the differences with the treatment of self-employed persons and also the treatment of entertainment expenditure.

The basic principle it is setting out is that in general, self-employed taxpayers cannot deduct meal expenses for income tax purposes. That is because they are treated as expenditure which is of a private nature. This is what they call the “private limitation” rule. Now, there are some certain limited circumstances where amounts expended on food could be deductible, such as where the requirements of the taxpayer’s business imposed extra meal costs such as a remote working location or unusual working hours.

The Interpretation Statement then goes on to explain there is a clear distinction between the treatment of self-employed taxpayers’ meal expenses compared with employees receiving meal allowances reimbursements while performing their duties. The latter is deductible expenditure to the employer and exempt income for the employee, not subject to FBT. The Interpretation Statement suggests self-employed persons may decide to operate through a closely held company and they become an employee of the company. In which case the same treatment applies. The reason given for this distinction is the different legal arrangements existing around these situations.

There’s also a difference in the treatment of entertainment expenditure. Entertainment expenditure generally for businesses is only 50% deductible. However, for the self-employed the Interpretation Statement considers the entertainment rules are overridden by the private limitation, so no deduction is available.

In relation to GST, where meal expenses are either private or domestic in nature for income tax purposes and non-deductible, then no GST input tax can be claimed. This is because they are being used for private and domestic purposes and not for making taxable supplies.

This Interpretation Statement is not going to be terribly welcome for self-employed taxpayers. It’s interesting to see this come out, but I wonder whether Inland Revenue will actually be devoting considerable energy into its implementation. But the rules are there and there’s a very clear if harsh distinction drawn between the self-employed and employees receiving meals allowances from their employer.

IRD Wellington is working from home

And finally, Inland Revenue, or at least its central Wellington office is homeless. The head office of Inland Revenue is in the Asteron building in Featherston Street, Wellington. About a thousand IR staff work there, mostly senior management, the policy and technical people and maybe some investigation staff. It’s not one of the big call centres dealing with the general public.

Anyway IR has closed the office and sent staff home after a new seismic assessment put the Asteron building at a lower level of earthquake compliance than previously thought. This is quite a major disruption, but thanks to Covid-19, we’ve got used to working from home. Inland Revenue certainly, yesterday ran a meeting that was scheduled without any particular interruptions.

Tongue in cheek now, I wonder if Inland Revenue might now be prepared to consider the treatment of remediation expenses a little bit more generously. This is an unclear area.

Fortunately, the reintroduction of depreciation does address a problem which had emerged where remediation expenses were considered non-deductible and were also non-depreciable, hence putting building owners under the pump. That’s been somewhat resolved by the reintroduction of building depreciation from 1st April 2020.

The Asteron building was apparently the largest office building in in Wellington. So that’s a significant loss. Seven floors are closed and one thousand staff, which is 20 per cent of Inland Revenue are now working from home. That’s going to be very disruptive. I hope it’s resolved very quickly because although we’ve got used to working from home there are benefits from working together and people will miss their colleagues. So anyway, good luck to the Inland Revenue staff affected. I hope this is sorted out pretty quickly.

Well, that’s it for today. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week ka kite āno!

New Zealand houses aren’t the only asset class that has exploded in value over the past 12 months. A report by the Secretary General of the OECD to the G20 finance ministers and central bank governors in Italy earlier this month noted that since he last reported to them in February 2021, the overall market capitalisation of virtual currencies has gone from just over US$1 tln to US$1.8 tln.

Now, quite apart from that near 80% increase, the growth has been almost five-fold since September 2020, when the market capitalisation was US$354 billion.

There are two things to note about this fantastic growth in value. Firstly it is going to attract keen interest from the tax authorities who will want their cut of the gains that have arisen. And of course, the tax authorities are still struggling to keep up with the pace of change in this sector. And Inland Revenue is no different from the rest.

There are some rulings in preparation at Inland Revenue including an updated release on how it views the treatment of cryptoassets. But its general position remains that cryptoassets will be taxable, with rare exceptions on the basis that rather akin to gold bullion, the value can only ever be released by sale, so therefore they must have been acquired with a purpose or intent of sale.

The thing is though, the whole cryptoassets sector is rapidly becoming ever more complex and new instruments are being developed, which point to Inland Revenue’s argument as not necessarily being sustainable. So that’s one point that people must be noting when preparing their tax returns for the year ended 31 March 2021. Now I’m sure we will see people coming forward who have substantial cryptoassets gains and are wishing to make the right tax declaration.

But the other matter, which is of concern to tax authorities, is trying to keep track of all of this. As is well known, the OECD has developed in recent years the Common Reporting Standards on the Automatic Exchange of Information. And what the Secretary General for the OECD said in his tax report to the G20 finance ministers and Reserve Bank governors, is that the OECD is designing a “tax reporting and exchange framework that will address the tax compliance risks associated with the emergence of cryptoassets and reflecting the crucial role the crypto exchanges play as intermediaries in the cryptoassets market.”

Now, the proposal is that basically they want to bring cryptoassets into the common reporting standards and in exchange for information. So that’s going to be quite complicated. One of the attractions of cryptoassets is they are supposedly off the grid or under the radar of the tax authorities, and, how shall we describe it, that the reporting requirements are a little bit more relaxed.

Anyway, the OECD is preparing detailed technical proposals on this, on a new tax reporting framework. And it is intending to deliver a proposal to the G20 later this year. As usual, we’ll bring you news on that when they when it happens.

After ten years, there is still confusion

Moving on, it is 10 years since compulsory zero rating of land transactions was introduced. From 1st of April 2011 most sales of land and buildings between GST registered persons became zero rated for GST purposes under what we now call compulsory zero rating provisions. If these apply, then the land transaction must be zero rated.

Now the provisions were introduced to prevent what was seen as a trend towards “Phoenix fraud”, whereby a vendor did not pay output tax on the sale of property to Inland Revenue but the purchaser claimed a GST refund. The suggestions were that the annual loss in GST was in the tens of millions of dollars.

Now, it’s important to note that this is between GST registered persons and what it did was fundamentally shifted the GST risk on transactions involving land buildings from Inland Revenue to the parties involved. And as an excellent little report on the matter from PWC points out, that wasn’t always fully appreciated by parties to transactions, particularly those who were seeking to claim an import tax deduction on the purchase.

After 10 years these rules should be relatively well known now. However, there’s still quite a lot of issues emerging on that. And I regularly encounter the issue where a GST registered purchaser has bought land from what they understood to be an unregistered person, only to find out afterwards that the vendor either is or should have been GST registered. Now that often comes up when they file a GST return and claim the input tax credit. Now, the result is they don’t get any input tax credit and that purchaser is understandably very upset. The last such case I handled the vendor finished up paying almost $400,000 as a consequence of getting that GST status wrong.

And it seems surprising this should be happening because the standard sale and purchase agreement does have specific provisions on the whole schedule declaring the GST status of the parties involved. I mean, one of the risks is that the GST position of one party depends on the GST profile or information of the other party. So it’s not often that that level of tax detail is required in tax transactions, but they are for compulsory zero rated land transactions.

The report from PWC has useful little tips for vendors and purchases. But the key point it makes is parties have got to take extra care with this. They’ve got to make sure that the GST status of both parties is absolutely clear and understood at the time the agreement was entered into. Otherwise subsequently, it gets very messy and expensive and the only people who win are lawyers and accountants with fees, trying to sort out the mess. Inland Revenue is quite happy about all of this because, as I said earlier, it has shifted the risk.

So generally speaking, if something goes wrong, it gets its cut and leaves it to the other parties in the transaction to sort themselves out. So again, pay attention if you’re involved in the purchase of land and buildings. It’s a compulsory zero rated transaction for GST purposes. Pay attention and make sure all the Is are dotted and the Ts are crossed.

A warning for trustees

And finally, just another reminder popped up with a new client coming to me this week, with a common issue, and that is the status of trustees who move to Australia.

Now as the Australian tax legislation for income tax purposes, deems a trust to be resident in Australia, if any trustee is a tax resident of Australia. So you could have a trust with seven, nine, 11, whatever number of trustees. But if one of those trustees is resident in Australia, then the trust is deemed to be resident in Australia and the consequences, particularly around capital gains tax, become potentially very severe.

There’s a slight anomaly in this position because often individuals that move from New Zealand to Australia qualify as what the Australian tax legislation calls a temporary resident.

And what that means is rather like our own transitional residence exemption. Non-Australian sourced income and gains are not taxable in Australia, but trusts are not covered, or companies are not covered by that exemption. So there is the situation where an individual who receives a distribution from a New Zealand trust is not going to be taxable on that in Australia, but if he is a trustee of that trust, making the distribution to him or her, then the trust is now within the Australian tax net.

So this new client is a reminder for anyone moving to Australia and they are either a trustee or have a power of appointment over trustees, then they need to resign as the trustee and revoke/transfer that power to another person who is not an Australian tax resident.

Given the sheer number of trusts we have in New Zealand, approximately half a million at last estimate, this is going to be a quite common scenario. So even if it is just a family trust holding a former residential family home in New Zealand, they could well be landed with a whole heap of Australian tax issues.

So anyone moving to Australia should take advice on the tax implications of you doing so and make full disclosures to your advisors. It is like the mess ups we see with the compulsory GST rating and land transactions. It’s astonishing how people are rather casual when explaining their circumstances to their advisers and often with very expensive consequences.

Well, that’s it for today. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients until next week, Ka kite āno.