This week has been a very busy week politically in the tax world, starting with a Cabinet reshuffle after David Parker relinquished his role as Minister of Revenue. In his own words, he felt that his position had become untenable in the wake of the decision by Prime Minister Chris Hipkins to rule out a wealth tax and capital gains tax for the foreseeable future.

Parker has been replaced by Barbara Edmonds, who has an interesting background in that she worked in Inland Revenue for some time prior to becoming an MP in 2020. In 2016 she was seconded from Inland Revenue to work as private Secretary to the then Ministers of Revenue, first Michael Woodhouse and then Judith Collins. (This is actually something that happens quite commonly with Inland Revenue officials working closely alongside other ministerial officials). In 2017, she then became a political adviser to Stuart Nash after he became Minister of Revenue. So, she’s got a very good background on the portfolio.

One of the things I think she might read with some amusement is what’s called a Briefing to Incoming Minister. Whenever there’s a change of minister the relevant department prepares a briefing to that minister, setting out their role and the key challenges ahead for as the particular ministry. I suspect Edmonds has been involved in preparing several of those. But this time she will be receiving one as recipient. The change is probably what you might call unforced, but it’s part of the fallout of the decision to not continue with the down the path of imposing a wealth or capital gains tax.

Signs of strain in the construction industry?

Moving on Inland Revenue has started a pilot programme to provide some support for those construction industry, or customers in the misguided terminology, in my view, of Inland Revenue. It’s intended to provide “tailored assistance” to help those in the industry through various stages of business. The intention is to have “meaningful discussions” with taxpayers in that industry about the business, how they’re doing, offering guidance and support about tax and entitlements. These will also involve “promoting the benefits of having a tax agent or bookkeeper”.

Long-time listeners of the podcast will know that when Inland Revenue was in the early stages of its Business Transformation program, tax agents felt, with some justification, that they’d been shut out of the process. It’s now interesting to see that Inland Revenue has realised that tax agents actually have a key role to play in the system and are encouraging their use. Good to see.

This is an interesting initiative by Inland Revenue. It probably speaks to strains that they are seeing within the construction sector, slow payments, people getting behind in tax debt, tax returns, etc.. This pilot program is an initiative to front foot those issues. I’m all in favour of Inland Revenue taking steps like this and moving forward I think it would be wrong to ever adopt the idea that any call from Inland Revenue is a bad call, that you’re in trouble. Sometimes they come in and they may have some suggestions about what to do and how to manage scenarios which can be very constructive.

In every case I’ve ever dealt with, if you front foot issues around slow payment, failure to file returns, whatever with Inland Revenue, you will find that they are receptive to those advances. A key part of their job is to promote voluntary compliance and help the smooth running of the system. As part of this it does matter if people can build trust that the Inland Revenue is actually, if not entirely on your side, a rather fairer referee than people might expect.

Te Pāti Māori go big on tax reform

Moving on, as I said, it’s been a busy week politically. We’ve had the effective resignation of David Parker as Minister of Revenue, and then yesterday Te Pāti Māori released their tax policy. Firstly you could not accuse them of being very limited in their ambition. In fact it’s a very ambitious policy.

The executive summary begins “We have a broken tax system in this country which has fuelled extreme wealth inequality that is only getting worse.” So, that’s the starting base point. In my view there are definite strains in the tax system, and we are seeing more and more of those emerge.

The key proposals are for GST to be removed from “kai”, lower income tax for those low incomes which is to be paid for by increasing income tax on those earning more than $200,000 and raising the company tax rate from 28% to 33% (also a Green Party proposal).

The key revenue raising measure, which is probably no surprise, is a wealth tax. As you know the Green Party also proposed a wealth tax on net wealth over $2 million. Under Te Pāti Māori’s proposals a 2% wealth tax on net wealth over $2 million is the starting point. However, if your net wealth is over $5 million, the rate is 4% and then if it’s over $10 million the rate rises to 8%.

From the work done for Treasury and Inland Revenue on the Government’s abortive wealth tax we have some idea of how many people might be affected by a wealth tax. An entry threshold of $3 million would have affected 99,000. The final design modelled for the Government was based on a $5 million threshold which would have affected 46,000 people. The report estimated the number of taxpayers who would have had net wealth in excess of $10 million as 16,000. So, it’s a pretty targeted group.

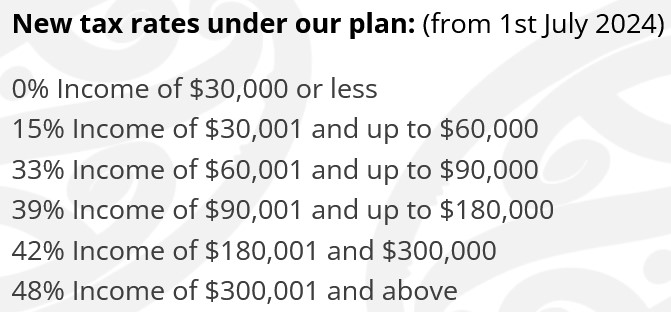

Te Pāti Māori have some fairly ambitious numbers on this. They believe that they their wealth tax would raise $23 billion per annum, which is a pretty significant amount of tax, in fact just a bit over 20% of the current tax take.

The wealth tax would be used to set income tax thresholds as follows:

Te Pāti Māori estimate 3.8 million people would benefit from their proposed tax cut package. They’re also, as I said, removing GST from “kai”. How that gets defined is going to be interesting and we’ll talk more about that in a minute.

There are several other new tax proposals. A proposed Overseas Financial Transfer Tax of 2%. This is to apply to overseas companies operating in New Zealand and will be additional to the company tax rate, which by the way, they propose increasing to 33%. This seems to represent some form of withholding tax. I imagine there might be quite a few double tax agreement issues involved in this.

A Land Banking Tax will be payable on all land that has not begun to be developed within four years of purchase. In addition, there will be a Vacant House Tax which would be payable on all properties that do not have a tenant after a six-month period.

Tackling tax evasion

One other interesting proposal is to tackle tax evasion which they say is “approximately $7 billion” annually. I think this number might also include tax avoidance which has an important distinction from tax evasion. Te Pāti Māori propose to invest $500 million into adequately resourcing the Serious Fraud Office and Inland Revenue to investigate and address these issues. This would be a colossal funding boost to both organisations. In the case of Inland Revenue, it would more than double its capacity and it would be a massive lift also for the Serious Fraud Office. So that’s an interesting one proposal, which is probably off the radar, but might be one of those things that actually gets pushed through when parties sit down to negotiate after the Election.

A Government leek?

Te Pāti Māori proposals got overshadowed by an apparent leak from within the Labour Party, immediately denied, that they were considering removing GST from food.

I’m often asked about the question of removing GST from food because on the face of it, it seems a fairly obvious thing to do. This happens in Australia and in many other GST/Value Added Tax (VAT) jurisdictions around the world food is zero rated to use the correct terminology. So if it can be done elsewhere, why can’t we do it here?

I’m in the group of tax policy advisers who are pretty much unanimous in thinking that after establishing a comprehensive GST, which included everything, we shouldn’t be tinkering too much around the edges and introducing exemptions, particularly ones such as food, which will turn out to be pretty costly. Te Pāti Māori estimates the cost of GST free kai to be between $3 and $5 billion.

Marshmallows and Max Jaffa

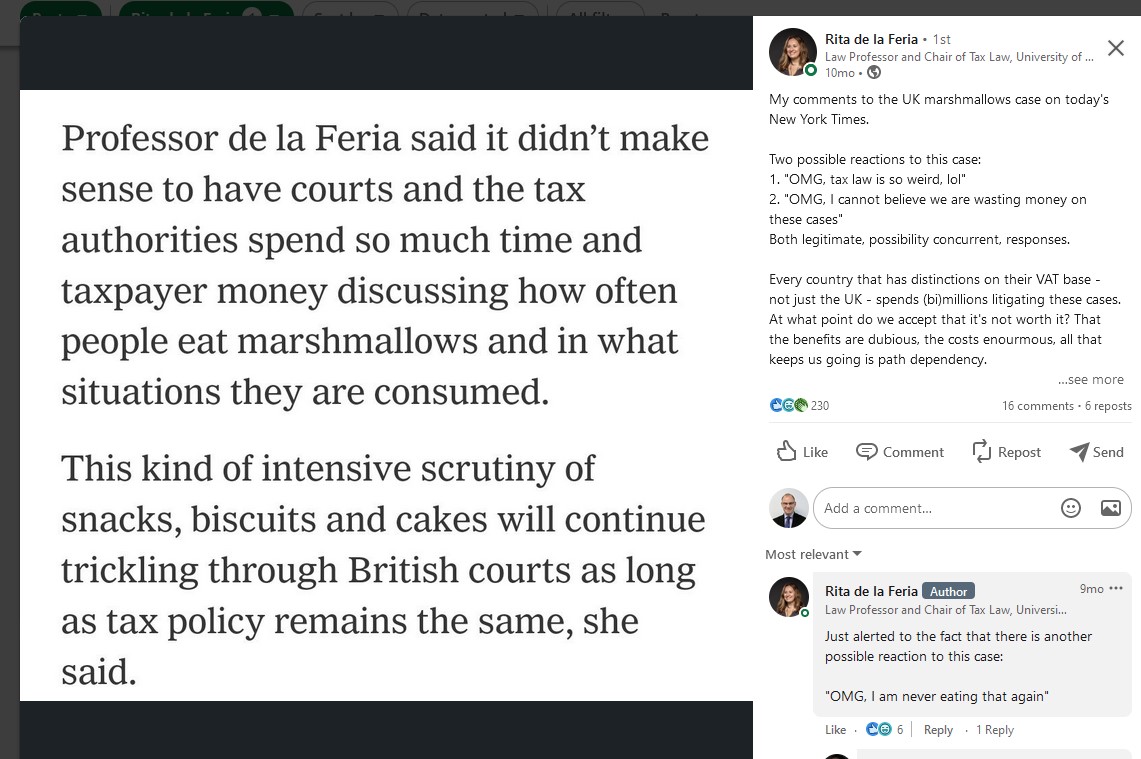

Our objections are firstly around the principle of not upsetting the purity of GST (and it’s one for which we get a fair bit of flak). There are actually really practical reasons around this matter. Like it or not, there are definitional issues around here and listeners to the podcast will recall when I discussed a recent UK VAT case involving marshmallows which because of their unusual size they qualified to be zero rated. There’s also the famous Max Jaffa VAT case which I explained on TVNZ on Friday.

Over in Australia they’ve had zero rating issues boundary issues around bread. In every jurisdiction around the world with GST/VAT these issues all arise. So, thinking because this is such a good thing to do, doesn’t bypass those problems.

Secondly, as I mentioned, it’s expensive. What do you do elsewhere? You’re giving away revenue as a tax cut so that’s got to be funded. In Britain, for example, the standard rate of VAT is 20%, and across Europe you will see rates of 20-25% and more as common. This trade off has to be taken into consideration, which is not considered too much by proponents.

And then finally, there is a very flawed assumptions that the full benefit of a cut will flow through to the customers. There is little evidence of that actually happening. The Tax Working Group looked at this issue and was not a fan.

Interestingly, the evidence it gathered from Europe was that whilst the majority of any general rate in cut in VAT (for example reducing the rate to 12.5%) did flow through to benefit consumers, in relation to specific incentives the estimate was that only 30% passed through.

Podcast listeners will know that I’ve cited Dan Neidle and Tax Policy Associates in the UK’s review of a couple of initiatives where VAT was reduced to zero. In one case the reduction in e-books, they saw no benefit passing through to consumers.

Well meant but poorly targeted policy?

Removing GST from fresh fruit and vegetables is a good example which VAT/GST specialist Professor Rita de la Feria of the University of Leeds has pointed out is a well-meant but ultimately poor policy.

Ultimately in my view the question about wanting to do something about cutting GST comes back to giving people some more money. Now we can do that through income tax cuts or with properly targeted payments to assist the low-income groups that are hardest hit.

This is something for our politicians to actually front up and address, because when you read the officials’ analysis (and it was in the papers relating to a tax-free allowance), they usually suggest it’s better to give more targeted reliefs in the form of direct benefits rather than widespread initiatives. And every time the politicians shy away from such proposals for whatever reason, maybe they think there’s no votes in it or whatever, but the principle still stands.

So, it will be interesting to see what Labour’s actual tax policies will be, whether they will run with removing GST on fresh fruit and vegetables. The proposal certainly seems popular.

But I’m actually quite glad to see political parties thinking big about tax and saying we need to do something radical in the area. Te Pāti Māori is the latest alongside Act, the Greens and TOP. All have made serious suggestions about significant changes to our tax system, whereas the two main parties seem to be just offering little more than fiddling around the margins. Anyway, we’ll no doubt see more in the coming weeks. And as always, we will bring you the news as it develops.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue has released a draft interpretation statement on the research and developments loss tax credits regime. This is a refundable tax credit available to eligible companies when they have a loss which has arisen from their eligible research and development expenditure.

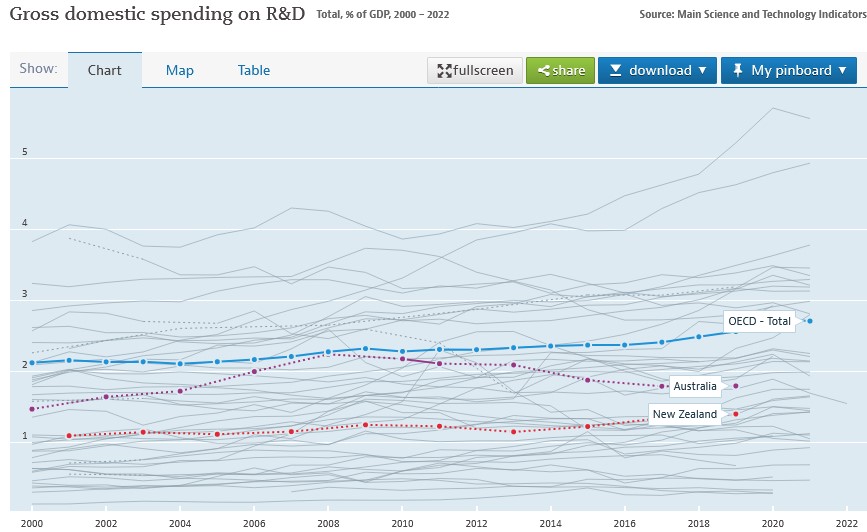

The regime was introduced in 2016 to encourage business innovation and also to address New Zealand’s poor record of R&D expenditure. According to OECD data, in 2019 New Zealand’s spending on R&D was just 1.4% of GDP, well below the OECD average of 2.56% of GDP. Over the past 20 years research and development in spending in New Zealand has been a full percentage point of GDP below the OECD average.

So given that we also have a poor record of productivity, increasing R&D expenditure is seen as critical in improving productivity and ultimately the strength of the economy.

That’s the background behind the introduction of the loss tax credits regime. It’s intended to assist the cash flow of those companies carrying out research and development. Often in the early years, these companies are running at a loss. Hopefully once the R&D matures and bears fruit, they will then have profits resulting from the expenditure.

But funding cash flow in those early years is pretty difficult. So instead of the tax losses to be used against future profits, under the regime, companies can instead receive a payment. Note, only companies can receive this R&D tax loss credit payment. That’s because losses incurred by partnerships, limited partnerships, look-through companies and sole traders can already pass those losses through to the underlying owners anyway, who will often be able to offset them against their other income. Essentially, they are already able to benefit from the ability to cash-up losses. But companies can’t do that, hence the introduction of the regime.

The Inland Revenue draft interpretation statement looks at the background to scheme, summarises the rationale for scheme and how it operates. A couple of key points about the regime: you can drop in and out of it, you can opt to choose a payment in one year but not in another year. Once you have claimed a refund by cashing up your losses, the regime operates rather like an interest free loan. You’re essentially required to repay it and it’s generally treated as being repaid when the company starts paying tax, the R&D having borne fruit.

However, there are other circumstances where the credit may have to be repaid earlier when there is, in the terminology of the regime, a loss recovery event. Now, that typically will happen if there’s a disposal or transfer of the intangible property, core technology, intellectual property, etc., which is done for either less than market value or the amount sold is a non-assessable capital gain.

Another situation, and this is actually one where I’ve been involved, is where the company is no longer tax resident in New Zealand. Some very interesting issues arise in that case. Then there’s the worst-case scenario, where a company goes into liquidation although what exactly can be recovered at that point is a moot point. But that’s still a loss recovery event.

And then finally, and similar to our other rules around the carry forward of losses and imputation credits, a loss recovery may occur if there is a loss of the required shareholder continuity. In the case of the tax loss credit regime, the relevant shareholding percentage is 10%. In other words, there’s no breach if at least 10% of the voting interests of the company are held by the same group of persons throughout the relevant period.

In my view this is a very important regime for improving the future productivity of the country. The scale of the spending is going on is quite interesting to see. We can get an idea of this because the Inland Revenue as part of the budget produces what is called a tax expenditure statement.

Tax expenditure statements are a summary of the cost of a particular tax preferred regime, which, like, for example, this regime, has been introduced for specific policy reasons. The OECD collects data on tax expenditures to get a global picture of what spending is going on in tax preferred regimes.

In the case of the R&D loss tax credit, the estimated value of the expenditure for the year to 30th June 2023 is $362 million, a little bit below 1% of GDP. The estimated expenditure for the year to June 2022 was $473 million. And you can see a steady rise since the regime was introduced in 2016.

Of course, the real importance of this regime is whether it has produced a boost in total R&D spending within the economy. And then ultimately, does that lead to increased productivity. It’ll be interesting to measure these once the data flows through in due course.

So, an interesting regime and good to see Inland Revenue give some guidance on this. It contains a few hooks but it’s well worth looking at if you’re thinking about trying to make use of the scheme. And as I said, we will watch with interest to see how it bears fruit.

Shuffling forward on internationalPillar One and Pillar Two proposals.

Moving on, we’ve talked fairly regularly about the OECD’s global minimum tax deal and Pillar One and Pillar Two. Last week the G20 met in India and the Secretary General of the OECD reported to the meeting that, “A historic milestone was reached at the 15th Plenary Meeting of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (Inclusive Framework) on 11 July 2023, as 138 members of the Inclusive Framework approved an Outcome Statement on the Two-Pillar Solution.”

In summary, what’s happened is that they’ve developed a text to a multilateral convention which will allow jurisdictions to exercise a domestic taxing right over the residual profits of the largest, most profitable multinationals. That’s what they call Amount A of Pillar One, and that will apply to multinationals with revenues in excess of €20 billion and profitability above 10%. What will happen is the scope of that taxing right will be 25% of the profit in excess of 10% of revenues. This €20 billion revenue threshold will gradually be lowered to €10 billion after seven years, conditional on the successful implementation of Amount A.

There’s a proposed framework for the simplified reporting application of arm’s length principle, which is key to transfer pricing and for baseline marketing and distribution activities. That’s what referred to as Amount B of Pillar One.

There’s a Subject to Tax Rule, again with an implementation framework, and this is really for developing countries to update their bilateral tax treaties to tax intra group income. This is where such income is subject to lower tax in another jurisdiction, in other words say one country has a 20% corporation tax rate. But that multinational shifts charges to another part of the multinational group in a jurisdiction where those charges are only taxed at a lower rate. This Subject to Tax Rule gives the first country more taxing rights in that income. Developing countries are very keen on this particular point because they feel that this is where the current tax regime has been almost predatory on their tax base.

There will be a comprehensive action plan developed by the OECD to “Support the swift and coordinated implementation of the Two Pillar Solution, coordinating with regional and international organisations”

On the face of it, all pretty much good news. But it’s interesting to read the views of those people who specialise in this field and there still seems to be quite a bit of uncertainty about whether in fact this whole thing will come to fruit.

In the meantime, for example, you’ve got lobbying going on in the United States. And it appears now that the US has managed to secure a further delay in the implementation of the Pillar Two global minimum tax 15% until 2026, according to a report coming out of the United States.

Pillar Two is the key proposal, because it applies to companies with annual revenues in excess of €750 million. Apparently, the US Treasury Department has managed to negotiate a delay in the implementation of this. It has got people watching all around the world as to what’s going on. It also means that the in the background, digital services taxes, for example, could still be ready to be deployed or introduced by jurisdictions if they feel that Pillar Two isn’t making enough progress and they want to secure their revenues. [Under the agreement just announced countries have agreed to hold off imposing “newly enacted” digital services taxes until after 31st December 2024.]

Overall, it’s a bit of a shuffling: one step forward, maybe half a step sideways and a quarter of a step back. In other words, progress is slow, but it’s still inching the way forward. Ultimately, it comes down to watching what happens in the United States and the lobbying goes on. If there’s a change of President next year all bets will be off at that point, I would say.

Smith, banged to rights, again. But should Companies Office be in the gun?

And finally, this week, the murderer and escapee, Philip John Smith, who’s been in jail since 1995 apart from the brief time he escaped to Brazil has now been sentenced to further two years imprisonment on tax fraud charges.

He was convicted for dishonestly using documents intending to gain pecuniary advantage, firstly, a application under the Small Business Cashflow Scheme and then for filing 17 false GST returns and a false income tax return. in total the attempted fraud was just over $66,000 of which was actually paid $53,593. He’s also been ordered to pay full reparations on that amount.

What he did was between October 2019 and March 2020, he registered five companies with the Companies Office with shareholders and directors, who were friends, associates or third parties unknown to him. He then he set up and activated myIR accounts for each company.

But Inland Revenue was quite quickly onto him, it seems, because it apparently detected the fraud involving the Small Business Cashflow Scheme in June 2020 only a few months after it started operating in April. So good quick work by Inland Revenue.

But the case also raises the point which an associate I bumped into this week mentioned, and that’s the actions (or inaction) of the Companies Office in allowing those five companies to get set up. New Zealand scores highly for ease of business in establishing companies. Many times, whenever I’m talking to overseas people, they are remarkably impressed about how quick it is to set up a company in New Zealand.

The question arises if people setting up companies by going directly through the Companies Office website, is it a little bit too easy? Was an opportunity to pick up Smith’s attempted fraud missed at that point by Companies Office? We don’t know. Accountants and lawyers are subject to the current anti-money laundering legislation, so we need to pay attention to what’s going on with company registrations and we have to obtain proof of ID. But my understanding is this process is a little less rigorous when you go directly through the Companies Office.

So good work by Inland Revenue picking it up quickly and catching Smith, again. But maybe some questions should be asked as to whether he should ever have been able to get that far along the line and that Companies Office should have picked it up sooner.

And finally, congratulations to the Football Ferns for their magnificent win last night at the start of the FIFA Women’s World Cup. I was lucky enough to be at Eden Park, which is why I might sound a little hoarse today! It was fantastic to experience such a great occasion even if the final nine minutes seemed like an hour. Congratulations again to everyone involved. Football definitely was the winner on the night!

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

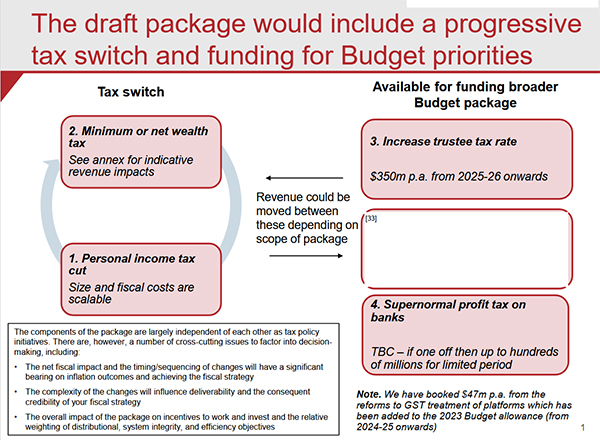

The big news last week was the release of the official advice to Ministers on tax incentives during the lead up to this year’s Budget. And it was quite a bombshell. Amongst the wealth of material provided was the surprising news that a key proposal had been until quite late in the piece a tax switch where in exchange for introducing a tax free threshold of $10,000, the Government would introduce a wealth tax.

Now, the Prime Minister immediately ruled out the wealth tax and also ruled out any capital gains tax if the government gets re-elected. So to a large extent, all this fascinating material is largely redundant. But it still provoked the continuing debate around the pros and cons of a wealth tax. And in fact, it’s really very interesting to go through the material and see how the policy developed and where they were planning to take it.

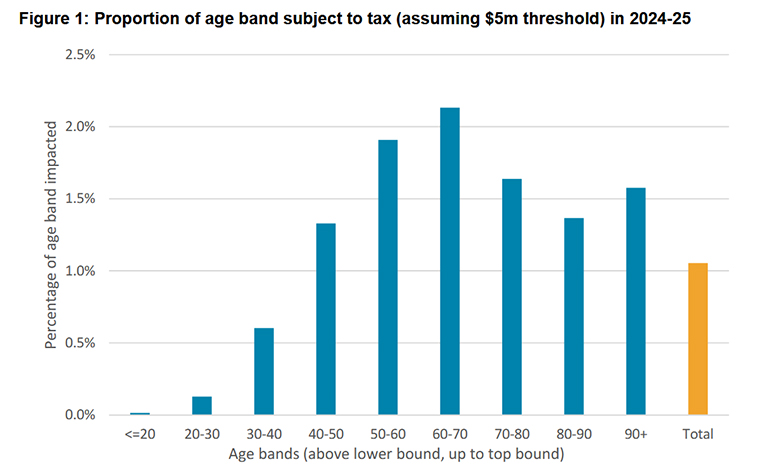

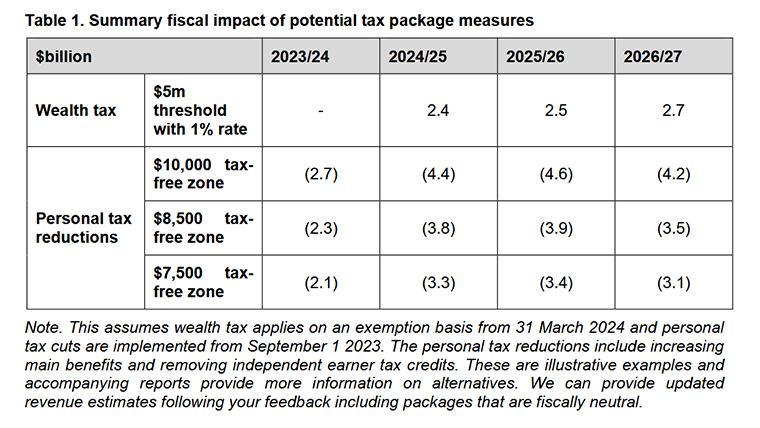

The final scheme would have applied a 1% tax rate to net wealth above a $5 million threshold under what was termed an “exemption approach”. This was initially thought it could raise between $2.7 and $2.9 billion annually and would have affected some 46,000 individuals. According to officials the wealth in scope at a $5 million threshold would be about $210 billion

A minimum tax?

Now, in the course of development the proposal started with something called a “minimum tax” under which proposal a person with high wealth would pay tax on the greater amount of either their deemed income calculated as a percentage of the net worth or the taxable income they have under existing income tax rules. The deemed income would have been based on the idea of economic income, which would include unrealised gains. If you recall when the Sapere report and the Inland Revenue High Wealth Individual research project were released, there was a great deal of controversy around this measurement because once you measured economic income and unrealised gains, it appeared the wealthy were paying an effective tax rate of 9%.

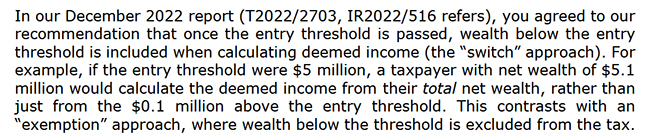

This minimum tax was the initial proposal which then got dropped over time. In the course of discussions, they moved away from what they called a “switch approach”. Under this once a person crossed the threshold, then all the deemed economic income would be subject to the wealth tax rather than just the proportion above the threshold.

And this so-called “exemption” is pretty much what we see in other wealth taxes around the world. It appears in the design of the wealth tax officials took a close look at the Norwegian system. One of the other features I found surprising was that the family home would be excluded. It seems to me that the tax preferred approach to the family home, has led to a large amount of overinvestment in housing.

Wealth taxes – profile of potential taxpayers

A key report on a wealth tax contained a very interesting discussion, around which group of taxpayers would be most affected. The projection was the age group which would be most affected at the $5 million threshold was that between 60 and 70. An estimated 2.1% of this group population has net worth over $5 million. According to these statistics, 1.5% of the over 90 year old group would be affected.

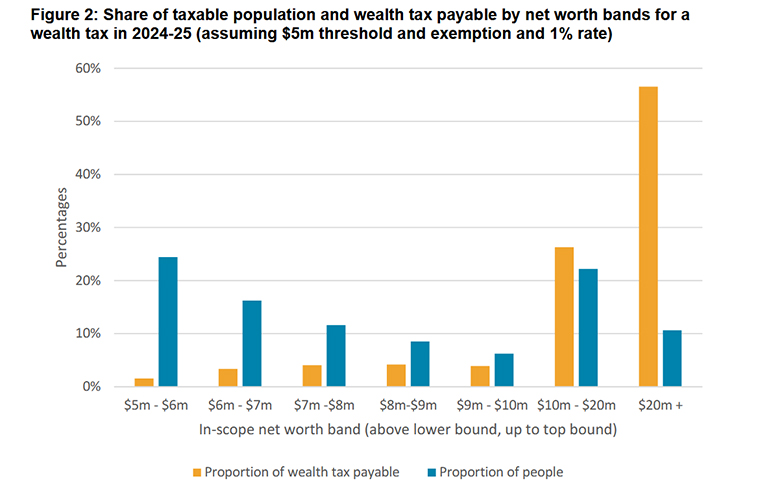

But in fact, as you might expect, more than half of the wealth tax would have been paid by the high net worth individuals with a net worth in excess of $20 million.

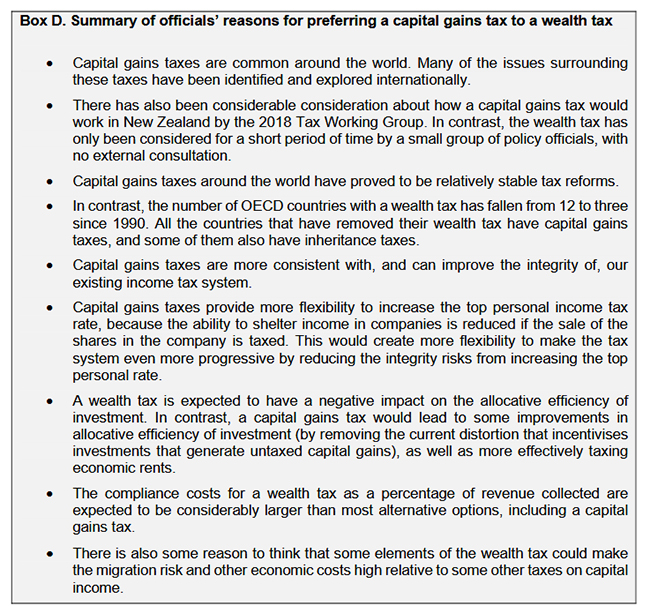

Officials prefer a capital gains tax

But I think the other thing that came out quite clearly from the papers was that the officials were not at all impressed by wealth taxes. They preferred a capital gains tax.

By the way, the officials view probably reflects a reasonably widely held belief if largely unspoken view amongst the tax community, that if we’re going to tax capital then a capital gains tax is probably the way forward.

Anyway politics intervened again and so a capital gains tax has now been ruled out in their prime ministerial lifetimes by two successive Labour prime ministers. However, as I said to Corin Dann on Morning Report the politicians may rule out capital gains taxes but we’ve got a lot of issues with an ageing demographic and the impact of climate change. The strains on the tax system, which have been recognised by Treasury and its Long Term Insights Briefing He Tirohanga Mokopuna in 2021 recognises that. The issues about needing more tax from somewhere haven’t gone away.

Paying for Cyclone Gabrielle

There were also suggestions as a one-off response to the impact of Cyclone Gabriel, for a levy on the banking sector. There was a comment that the four main banks have persistently “elevated levels of profitability relative to the smaller New Zealand banks and overseas and comparators in part due to the relatively low costs of the large New Zealand banks.” A temporary levy on the banks could raise somewhere between $230 and $700 million. As the Greens noted, Margaret Thatcher of all people did actually impose a surcharge on banking excess banking profits when she was Prime Minister.

There was also a suggestion of a one-off flood levy similar to what was introduced in Queensland following their catastrophic floods in 2010-11. A temporary 1% levy applied to all taxpayers would have raised $1.8 billion. But one only applied to income above $100,000 would raise $250 million.

The quid pro quo – a tax-free threshold

The quid pro quo for a wealth tax would have been a $10,000 tax free threshold. Once again Treasury and Inland Revenue weren’t enthusiastic. They suggested more significant increases in the lower thresholds including lifting the threshold at which the rate goes from 10.5 to 17.5% from $14,000 to $25,000, which is actually substantially ahead of where it would have been if had it been indexed to inflation. However, they proposed lifting the next threshold rate increases to 30% to $52,000. This is the threshold which I think is extremely problematical because of the large jump and at its current level of $48,000 is now well below both average and median wages.

There are two things of interest here. Firstly, a recognition that something has to be done. Tax free thresholds are very popular, but they’re not as efficient is the official advice. Secondly the cost of increasing these thresholds would have been over $4 billion annually. This is an acknowledgement that by not indexing thresholds since 2010, governments have given themselves a permanent headache around having to make threshold adjustments that become increasingly expensive.

A mystery policy?

A tax-free threshold is apparently out of the question. But maybe not because amidst all the papers, there’s are parts which have been redacted. These refer to another policy, whether that was capital gains tax, we don’t know. But whatever it was, it’s been redacted and not been released under the Official Information Act.

We’re now within three months of the General Election and Labour is still to release its tax policy. So maybe there’s something in that hidden part which will be revealed.

Secrecy and the Generic Tax Policy Process

There’s been some discussion that because this was all carried out secretly and outside the Generic Tax Policy Process (GTPP) that maybe this might not have resulted in a terribly efficient tax. I’m less concerned about governments deciding they’re going to do something for electoral gain and requesting work be carried out discreetly. But I do agree that if it’s done outside the GTPP, there is a risk that the design could be faulty. We’ve seen that with the bright-line test and the continual tinkering that has to be done. Worth remembering, by the way, that the bright-line test itself was a surprise. There was no previous consultation before it was first introduced in the May 2015 Budget by Bill English.

I like tax surprises in budgets, and I believe they’re part of normal politics. As I’ve said before, tax IS politics. But I do think that if you look entirely at tax through a political lens, then you start to get this narrow view developing right now where everyone says the politics of raising taxes are too hard, but the economic question of, how are we going to pay for the coming challenges just gets sidelined.

To repeat myself, we have serious issues to address coming up. And my view is if you want to maintain the broad based, low rate approach to fund these challenges, you’re going to have to do something around capital taxation. And the sooner you do it, the better.

Inland Revenue dropping the ball on investigations?

Moving on, one of the officials’ key objections to a wealth tax was the cost of compliance. Inland Revenue would clearly need to increase its capabilities. In its advice on its Initiative Work Programme it commented “the Government’s current tax and social policy work programme will use up most of our specialist design and delivery capacity over the next three years.”

Now the question of Inland Revenue’s operational capabilities came up at the start of last week when it was raised by National’s revenue spokesperson Andrew Bayly.

Following some written questions to the Minister of Revenue, he had determined that the number of investigations conducted by Inland Revenue dropped from an average of 77 a month between February 2017 and October 2020 to only 17 a month between October 2020 and June 2022. Furthermore, the time Inland Revenue spent on hidden economy investigations has also dropped substantially, from 3094 hours in November 2020 to just 805 hours in May this year.

Mr Bayly thinks Inland Revenue is dropping the ball here. Now, he’s tried that for obvious political reasons to Inland Revenue’s work on the High Wealth Individual research project, but that was separately funded. (Incidentally, early drafts of the report were made available to Cabinet as part of the pre-budget preliminaries).

There is an ongoing operational issue, in my view, about Inland Revenue’s investigations activity. And actually, it has acknowledged it has not been doing as much work in the investigations and debt recovery field. Page 36 of its Annual Report for the year ended 30 June 2022 notes:

“We did less work than would be typical in areas such as debt collection, investigations, disputes, litigation and liquidation activity.”

Now, part of this is down to the response to COVID. There were great demands made of Inland Revenue to which it responded superbly. But note the number of investigation hours back in November 2020, which is in the heart of the pandemic, was 3,094 but now it’s down to only 805 hours when we’re supposedly post pandemic, or rather a different stage of response to it. Inland Revenue saying that the fall off in investigations is because it has had to deal with COVID and this year’s weather-related events is not a satisfactory explanation in my view.

And when you start digging into Inland Revenue’s appropriation statements which are published as part of its annual report, you can see the amount spent on investigations for the past five years has fallen quite considerably in absolute terms, let alone when adjusted for the impact of inflation.

Reduced investigation funding

In the year to June 2018, the investigations appropriation was just over $140 million. But for the year to June 2022, it was just over $113 million. That’s a significant drop of nearly 20% in absolute terms.

Inland Revenue investigations appropriation per annual reports.

30 June 2022 $113.235 million

30 June 2021 $124.325 million

30 June 2020 $109.720 million

30 June 2019 $134.706 million

30 June 2018 $140.164 million

So, what this points to is the claims being made by Mr Bayly about Inland Revenue taking its eye off the investigations ball does appear to be backed up by the evidence of where it’s been spending its money. One of the explanations for this appears to be tied into its massive Business Transformation project. Inland Revenue, once it got started on this, seems to have pretty much solely focused on getting it across the line.

Where did the investigations staff go?

Part of Business Transformation included substantial reductions in its headcount, which went from 5789 in June 2016 to 3923 in June 2022. Now, that’s nearly a third of the workforce gone. We also know that although there was a substantial number of staff (nearly 800 apparently) whose sole purpose was simply re-inputting data so it could be used, a large number of very experienced investigation and operational staff were also let go. I know that because I’ve been speaking to a few of them.

Therefore, other tax advisers and agents and I are wondering whether Inland Revenue now has a diminished Investigation capability. There’s also another matter which Andrew Bayly also picked up on, the fact that Inland Revenue has decided to adopt a completely new metric for measuring its investigation performance. That makes you wonder why it’s done that. We won’t know what they’re measuring and how effectively, as the year just ended on 30th June is the baseline for this new metric.

But it’s important in a system that relies on voluntary compliance, there is the expectation by all of those taxpayers who comply that Inland Revenue is making sure that those who are not playing by the rules will be found and investigated. The concern is if Inland Revenue’s capacity to do that is diminished and it’s not fulfilling that role, then the overall perception of the integrity of the tax system is undermined. And that’s not good long term because naturally people will start thinking “That person is getting away with it, so we can too”.

I hope this is something the new Commissioner of Inland Revenue Peter Mersi is paying a lot of attention to. It will be very interesting to see what the department says when its latest annual report is published in October.

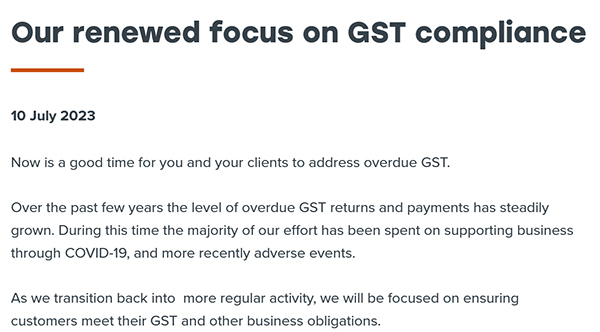

Inland Revenue renews its focus on GST

And finally, this week and, coincidentally or not, a couple of days after the story about Inland Revenue’s lack of investigation focus, it posted a warning for tax agents about “Its renewed focus on GST compliance”

Now, you can easily interpret this as an implicit acknowledgement of Andrew Bayly’s criticisms, but it is in fact another sign which we’ve seen steadily emerging that Inland Revenue is now repositioning itself back into what you might call its regular routine.

As usual, we’ll keep an eye on what that means and bring you developments as they emerge.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Submissions close next Friday on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the tax bill introduced alongside the Budget. The bill, as is typical, sets the annual rates for the current year ending 31st March 2024, but also has key provisions relating to the establishment of the legislative basis for the implementation of the Pillar Two international tax proposals at a later date. Separately, there are key provisions for increasing the trustee tax rate from 33% to 39%, with effect from 1st April next year.

The main part of the bill involves preparing the groundwork for the OECD’s Pillar Two multinational tax proposals. These are part of the Global Base Erosion and Profit Shifting (BEPS) initiative which is intended to introduce a global minimum corporate tax rate of 15%. Now, I generally have no involvement with clients that would be affected by these proposals which are targeted at the large multinationals. Most of the clients I deal with on international affairs are much, much smaller scale operations.

But there will be plenty of expert commentary and submissions on this particular bill because it will affect significantly large multinationals, those with international presence and gross turnover exceeding €750 million annually in any two of the preceding four years. It’s a fairly select group. There may be some tweaks as a result of submissions being made, but I would expect this to go through largely unchanged. But it will be interesting to see what submissions are made around this.

Increasing the trustee tax rate – maybe not quite such an obvious move

Of much more direct interest to many more clients and probably also much more controversial is the proposal to raise the trustee tax rate from 33% to 39%.

Now, conceptually aligning the trustee tax rate with the top personal income tax rate makes sense. We see that in other jurisdictions. Practically speaking, however, given the incredibly diverse and prolific nature of trusts in New Zealand, this would seem to be a much more practically difficult issue to implement it.

In discussions with other advisors, a couple of points have emerged. There seems to be a general consensus that some form of de minimis threshold is appropriate to take account of the fact that there are so many more trusts and they have operated on a policy of not generally distributing income because the 33% tax rate probably aligned with most of the income tax rates applicable to most of the beneficiaries. The 39% tax rate only kicks in above $180,000 income and that’s a much smaller group.

The argument which has been raised is that the measure, although conceptually correct, is actually in response to a small group. And therefore, it has a rather indiscriminate effect on people whose aggregate income including that of a trust, would not cross the $180,000 threshold. The suggestion has been made that we should have some form of de minimis threshold. I’ve seen suggestions raising between $15 and $50,000.

In response to this proposal Inland Revenue officials have asked “What’s to stop people setting up a number of trusts to maximise the advantage of the differing thresholds?” Well, two things. One, first of all, practically the cost involved of establishing these trusts, you would typically not get much change out $2-3,000 plus GST. But more importantly, you then have ongoing costs involved because following the Trusts Act 2019 coming into force in early 2021, trustees are much more conscious of their obligations including providing information to beneficiaries.

But more importantly, if someone established ten trusts like that and then divided up assets and income producing assets so as to maximise any potential threshold that would run square head on into Inland Revenue’s existing anti-avoidance provisions. Therefore, in practical terms, I think Inland Revenue’s arguments about the risk aren’t really a starter. There is also the question that there are there are increasing compliance costs involved with running trusts now as I just mentioned.

There’s also something Inland Revenue tends to glide around in my view and that’s its very, very narrow view of Section 6A of the Tax Administration Act. This states Inland Revenue’s duty is to collect the highest amount of revenue that is practicable over time, bearing in mind the costs of compliance. Keeping that in mind some form of de minimis seems a not reasonable approach. Otherwise, trustees may feel that they are obliged to do a load of distributions to beneficiaries just to minimise the tax payable.

I have actually encountered scenarios where trusts were established which could have done that and minimise the tax payable but didn’t do so for a variety of reasons. So it could be that inadvertently Inland Revenue may trigger the trustees to actually distribute income at lower tax rates than they were doing previously. I’m certainly watching to see how the Select Committee responds to this point.

Deceased estates potentially unfairly penalised?

The second point about the 39% tax rate increase is how it will apply to estates of deceased persons. The proposal is the 39% rate will apply to a deceased estate after 12 months have passed since the person died. Now, my immediate reaction to that proposal when I read it was that period was way too short, and that has been confirmed in subsequent discussions with other tax practitioners and lawyers. In fact, right now I’m involved with the tax affairs of an estate where more than three years has passed since the death of the deceased person.

The majority view of the lawyers I’ve spoken to on the matter is the minimum period should be at least 24 months and probably somewhere between 36 and 48 months would be much more realistic. I would be interested to see what happens here; particularly about just how many law firms do make submissions on this. I’ve made the law firms I work with aware of the issue and recommend they do submit. Select committees sometimes hear a lot from the same people, but they are always particularly interested in hearing from people who don’t normally submit but are doing so in this case on the practical basis “Our experience is this would be not a good move” or “We would support it”, whatever.

Anyway, submissions on this bill close next Friday. If you have concerns about any of these measures I’ve discussed, make a submission to the Finance and Expenditure Select Committee using this link.

The IMF holds forth on cryptocurrencies

Now moving on, this week the International Monetary Fund, the IMF, released a working paper on the taxation of crypto currencies. https://www.imf.org/en/Publications/WP/Issues/2023/06/30/Taxing-Cryptoc… This is an absolutely fascinating paper, it’s actually one of the most interesting papers on the taxation of cryptocurrencies than I have seen since crypto assets moved into the mainstream over the last five years.

In short, the IMF’s view is that tax systems need updating to handle the challenges posed by crypto assets, particularly in relation to their anonymity and their decentralised nature. And these, in the IMF’s view, make it hard to establish and maintain effective third-party reporting systems such as we use here in the banks or the international OECD’s Common Reporting Standards on the Automatic Exchange of Information.

It’s a very readable paper which starts by pointing out that after basically starting from zero in 2008, the market value of crypto assets peaked in November 2021 at about USD3 trillion USD (nearly NZD5 trillion). Although estimates vary because the surveys are self-selected, maybe perhaps 20% of the adult population in the U.S. and 10% of the adults in the U.K. hold or have held crypto assets. And the number of global users could be as many as 400 million people. On the other hand, although USD3 trillion sounds like a lot, it’s only about 3% of the global value of equities.

But the paper notes the potential for disruption, which is one of the founding ethos of Bitcoin and the crypto asset world, is quite significant. There are all sorts of questions around the tax impact of all these colossal capital gains suddenly arising and then the potential impact of losses, now that USD 3 trillion valuation is down to around $1 trillion. What’s going to happen with those $2 trillion of losses? Are they being claimed?

The paper really is very, very interesting in covering a whole number of topics. And basically it sums up the problem as being tax systems were not designed for a world in which assets could be traded and transactions completed in anything other than national currencies. It has some interesting comments about the effect of crypto billionaires. Apparently 19 were on the Forbes list, the richest list in America in April 2022. In an interesting aside the paper comments about “a loosely defined sense that much wealth channelled into crypto escapes proper taxation appears to have become part of the wider mood of dissatisfaction around the taxation of the rich.”

Blockchain efficiencies for tax administrations?

Yes, there are certainly crypto billionaires, but a lot of ordinary people probably piled into crypto because they saw an opportunity to realise substantial gains. How they declare those is of course where this paper is focussed on. It also notes that much is made of blockchain technology and it the working paper notes that the information blockchains contain on the history of transactions is actually remarkably transparent which

“might ultimately prove valuable for tax administration; and the use of smart contracts (self-executing programs) within blockchains, for example, might in principle help secure chains of VAT compliance and enforce withholding.”

What this paper picks up on is concerns I haven’t seen too much discussion of around the VAT (value added tax) or GST consequences of transactions using crypto. The paper’s section on externalities picks up on an issue which has is often raised in relation to crypto, and that’s the carbon effect of mining. It notes that the associated carbon emissions are cause for considerable concern including an estimate that in 2021 Bitcoin and Ethereum mining used more electricity than either Bangladesh or Belgium and were responsible for generating 0.28% of global greenhouse gas emissions. It suggests there maybe should be a charge on mining in relation to that effect.

Overall, the paper does not propose solutions. It is a working paper which is really raising all the issues. Now, it notes which I’ve mentioned recently, that the OECD has introduced its Crypto-Asset Reporting Framework, which is to extend the Common Reporting Standards reporting to the crypto world. But in the IMF’s view, “implementation remains some way in the future and in any case will not in itself resolve the issues challenges proposal posed by decentralised trading.”

Overall, a very comprehensive and readable paper which brings a big picture thinking to the issues the taxation of crypto crypto presents. I highly recommend reading it.

Government tax revenue behind forecast

And finally this week, the Government released its financial statements for the 11 months to 31st May. Of note immediately was that total tax revenue of $102.8 billion was $2 billion below forecast. Now $1.87 billion of that shortfall related to lower corporate income tax. GST was also $104 million below forecast and also another note that the economy is slowing down.

On the other hand, the rise in interest rates means that the amount of resident withholding tax collected on interest is $242 million ahead of forecast. Incidentally, the withholding taxes on dividends are also $12 million higher than forecast. That latter point may be in reference to what we discussed at the opening of the podcast, with the trustee tax rate rising to 39%, some more dividends are being paid ahead of that rate taking effect.

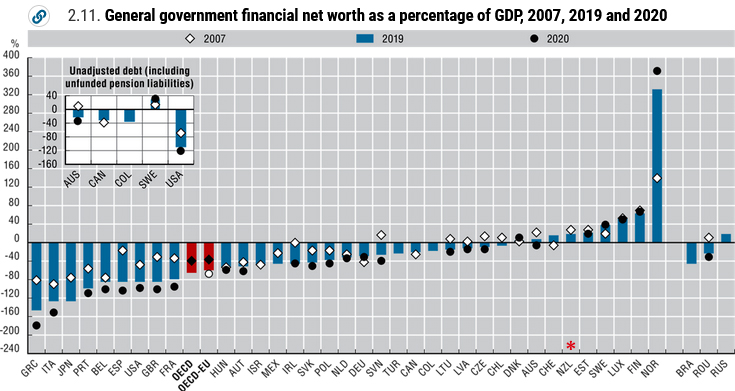

Government core expenses at $145.6 billion were actually $120 million below forecast. Interest costs were just under $6.6 billion, $134 million higher than the Budget estimate. Overall, the government debt rose by $5.1 billion to $73.3 billion, but net that’s the equivalent of 18.9% of GDP. The Government is still in the black. Overall, based on 2021 numbers, its net worth of $170.4 billion, which is roughly 44% of GDP, keeps it as one of the few OECD countries with a positive net worth.

There’ll be plenty of talk about budget deficits, etc. going forward in the election campaign. And we’ll be paying attention to what the parties say on tax. But it’s probably just worthwhile keeping it in context that the Government’s balance sheet is reasonably solid. You wouldn’t want it to be running away rapidly, but when you look at what’s going on in the United States where they basically cobbled together ad lib budgets to just paper over the cracks until the next crisis emerges, we are in a reasonably strong position.

How that balance sheet is maintained and used to brace ourselves for the impact of climate change is a major challenge. I think we now have a major issue in terms of having to basically fund adaptation by having to fund moving people out of at-risk areas. Cyclone Gabrielle rendered 700 homes unliveable. That could add up to maybe a billion dollars. Although a billion dollars in the context of $145 billion government spending is well under 1%, a billion dollars year in, year out is money that is not going into other areas that people want for health, education, etc. So anyway, the Government’s books are in reasonably good shape, but there are strains ahead.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

As is well known, income tax thresholds have not been increased since October 2010. What also gets overlooked is that the GST threshold of $60,000 was last adjusted in April 2009. And this week, Stuff ran a story about Kristen Murray, who has petitioned Parliament to have the GST threshold increased to $75,000.

She argued in her petition that the lower threshold is crippling small businesses. Inland Revenue disagrees but Kristen has gained the support of BusinessNZ, who supports regular indexation of tax thresholds.

A BusinessNZ economist noted that the effect of inflation means that the $60,000 threshold set back in 1 April 2009 should now be roughly about $82,000. Now the driving principle of the GST system is a broad based, low-rate principal approach and a reasonably low threshold is consistent with that approach.

GST came into effect on the 1st of October 1986 and the threshold set then was $24,000.

Looking at the table above it has actually more or less kept pace with inflation based on where it started – until now.

Notwithstanding that, given that it’s now 14 years since it was last adjusted, some form of increase to the threshold is not unreasonable. And the number of businesses a threshold change could affect is quite significant.

According to Inland Revenue data supplied to Parliament’s Finance and Expenditure Committee in 2022 there were 264,457 taxpayers who are GST registered, but with turnover of $60,000 or less. There’s another 27,000 or so with turnover between $60 and $75,000. So, as we said, increasing the GST threshold could take a large number of taxpayers theoretically out of the GST net.

But GST has an interesting effect and it’s also seen officially as a main pillar against tax evasion because of its comprehensive nature. Pretty much everyone finishes up paying GST somewhere along the line, even those within the cash economy. They still finish up paying GST when they’re purchasing supplies, food, petrol and the like. So, there would be a natural reluctance on the part of Inland Revenue to increase that threshold substantially. But to repeat an earlier point after 14 years, it’s not unreasonable.

By the way, Kristen’s suggested $75,000 threshold would actually bring it in line to the Australian threshold, which is A$75,000. I think one of the things they could also borrow from Australia is perhaps allow for quarterly GST returns.

There are therefore risks about the GST threshold being too high and the base being narrowed, but if they kept it too low then businesses may deliberately hold back from growing and crossing the GST registration threshold.

Over in the UK, where the equivalent of GST, value added tax or VAT, registration threshold is £85,000, there is in fact a very noticeable drop-off effect around that threshold.

The reason possibly might be because once you are VAT registered, you’re charging VAT at 20%, so businesses that can’t see themselves growing substantially quickly pass that threshold may be quite reluctant to effectively increase prices by 20%.

Now, I’m not aware of any such evidence here in New Zealand. And I think the issue, which Kristen pointed out, compliance is a bigger issue for micro-businesses. With compliance there comes a point where there is an irreducible minimum. Whether we’re at that point there know I don’t know. As I mentioned earlier, offering opportunities around quarterly reporting would perhaps help. And these days, the advent of software programs such as Xero, MYOB, and Hnry do help micro-businesses manage their tax much more effectively.

But in terms of GST and tax administration, I think the next big step would be to zero rate all supplies between GST registered businesses. That would help put an end to the merry go round which goes on right now where a GST registered business charges another GST registered business GST, collects and pays that GST to Inland Revenue, while the GST registered business, which has just paid GST, then claims it back from Inland Revenue. Overall, there’s no net GST effect. I therefore think moving to zero rate such B2B transactions is a logical step. How far away that is, I don’t know. It doesn’t appear to be on Inland Revenue’s work programme at this point.

At the moment, we’re left with the only other adjustment that might help microbusinesses would be to increase the GST threshold. As I said, my view is something like that should happen soon, but we’ll have to just wait and see.

Airbnb, GST and unintended consequences

Moving on, and still on GST, I came across a case this week where a residential property owner couldn’t let the property so decided to change his approach and started letting it out as an Airbnb. Airbnb letting represents taxable supplies for GST purposes. He was GST registered for another activity and he did include the Airbnb income in his GST returns.

The issue has now popped up that he wants to sell the property. And it looks like unless he is selling to a GST registered person when compulsory zero rating will apply, then he has inadvertently given himself a GST problem. If he sells the property, which remember was originally a residential property to a non-GST registered purchaser, the sale price the price will become GST inclusive, which basically will bite into his margin.

This is a good example of paying attention to what’s going on around your activities and that you should always seek advice when you propose to do something that may have GST implications. Tax is full of unintended consequences and for this particular taxpayer, I’m afraid there probably is a huge unintended consequence of basically surrendering the equivalent of 13% (the GST inclusive portion of the sale price) on a residential property sale. He was already carrying on a GST activity already and Airbnb just represented additional taxable supplies. So, for anyone thinking of switching from residential property letting to Airbnb that’s a trap to watch out for.

The Great Tax Debate – “Think of the consulting fees!”

And finally, on Friday night I was part of the Great Tax Debate organised by the Tax Policy Charitable Trust, where I and several other tax practitioners debated the proposition: A wealth tax is the best solution to wealth inequality.

I was the leader of the affirmative team, and I was ably assisted by Mat McKay of Bell Gully and Sladjana Freakley of EY. Opposing us were Robyn Walker of Deloitte, Simon Coosa of Minter Ellison, Rudd Watts and Jeremy Beckham of KPMG. Professor John Prebble, one of THE gurus of New Zealand tax, chaired the debate. We had a lot of fun on the topic including an interesting Q&A session where someone asked, “Has EY gone woke?” The answer, of course, is no.

In the end thanks mainly to some pretty shameless populism including an appeal to the base instinct of the tax consultants in the audience, “Think of the consulting fees!”, we in the affirmative team sneaked home. Before the debate started everyone was asked to register their position as a yay or nay. And then the net movement from that would determine the winner. And we managed to move the dial several points in our favour. But before the Green Party start jumping up and down celebrating “We told you people wanted a wealth tax”, over 60% were still against a wealth tax.

As I said, it was a lot of fun with plenty of laughs all around. The question about whether EY has gone woke raising one of the bigger laughs. I’d like to thank the organisers, the Tax Policy Charitable Trust, hosts Bell Gully, Professor Prebble, my team-mates, Mat and Sladjana and our opponents, Robyn, Simon and Jeremy together with the 80 plus attendees in the audience for a fun night. We hope to see more of these debates in the future.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.