17 Aug, 2022 | The Week in Tax

- Insights from the Budget information release

- The IRS is a big winner in Biden’s tax proposals

- Inland Revenue writes off $100 million

Transcript

The Budget information document release on Thursday caused a bit of a stir and some excitable commentary. A few points stood out for me, particularly in relation to the ongoing controversy over the cost-of-living payment and its delivery by Inland Revenue.

We already knew Inland Revenue was less than happy to be involved in it, but some of the further documents released shed further light on it. Treasury’s recommendation was,

“…if you wish to progress with the payment along the lines of the commission[sic], the Treasury recommends that Inland Revenue be the delivery agency, given they are the agency best placed to deliver such a broad payment in the short term.”

Inland Revenue, on the other hand, didn’t want to be involved because,

“…delivering this payment, which is estimated to require around 1,000 staff at its peak for around two months, would have critical operational impacts on Inland Revenue while delivering the current COVID 19 economic supports. The addition of this payment to the portfolio of services that Inland Revenue already delivers would severely compromise Inland Revenue’s already stretched workforce.”

That’s quite an admission from Inland Revenue. I guess some of the controversy about accidental overpayments of the cost-of-living payment to ineligible recipients is an assumption that Inland Revenue is highly efficient. In reality once humans are involved then on the precept of “garbage in, garbage out” there were always going to be a few errors involved.

What concerns me about Inland Revenue’s admission, though, is it does seem to point to perhaps the organisation is a little bit too lean and mean after its staff has been cut quite substantially by over 20%. We know it makes extensive use of contractors which as we discussed last year, led to an Employment Court case, which it won, by the way. On the other hand the admission that basically it needs to increase its staff by about 20% to manage something like this points to perhaps Inland Revenue being more stretched than it ought to be in staffing levels.

And that also indirectly does raise some questions about Inland Revenue’s enhanced capability following completion of its Business Transformation project. It is perhaps too simplistic to think that a couple of pushes of buttons is all that was needed to enable the cost-of-living payments to be made. But it does strike me as surprising that Inland Revenue has to devote a thousand staff and additional resources to deliver the payment.

Now, one of the other criticisms that emerged has been made about the payment is that only 1.3 million people have received it so far of the estimated 2.1 million. But in reality, it was known beforehand that all 2.1 million estimated eligible people would not receive a payment straight away. One of the papers notes,

“around 25% of potentially eligible recipients, around 500,000 individuals, will not receive this payment during the proposed August to October window because their assessment for the 2020 122 tax year is not complete”.

The paper goes on to explain that based on tax filing information for the year ended 31st March 2020,

“…around 38% of people who submitted an IR3 did so by the end of July, and 53% by the end of September 2020. Assuming the same pattern for the 2021/22 tax year, Inland Revenue expects there will be a long tail of IR3 filers who would not receive their cost-of-living payment during the proposed payment window.”

The paper notes this will mean Inland Revenue will have “increased contacts” as people will be asking why they haven’t received a payment. This will then “have an impact on other services for taxpayers” such as Working for Families.

This is quite a reasonable point. But, of course, politics has intervened. And when you’re beating a dog, any old stick will do. So, the Government is copping it for what was obviously something that would have happened in the first place.

The other point that comes across is a wider one around the future sustainability of the tax system. Treasury was pouring a lot of cold water on Ministers’ various spending plans and pointing out the unsustainability of what was being asked for. Treasury warned

“Meeting these new targets consistently will require you to maintain a balance between revenue and expenditure. Over the medium term this would require significantly constraining spending growth, unless your revenue strategy is adjusted to maintain a higher level of tax revenue-to-GDP in later years.”

As the Herald noted, that would mean finding new taxes to leave spending as a share of the economy higher over the long term.

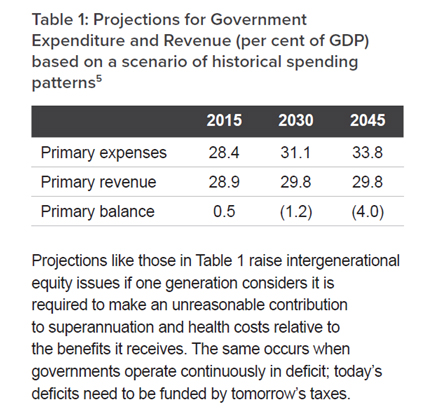

Now, one of the reasons the Tax Working Group recommended a capital gains tax was it had considered the long-term fiscal sustainability of the tax system based on the then current spending trends. Its Submissions Background Paper in March 2018 pointed out that based on then current projections, the Government’s primary expenses would rise steadily to reach 31.1% of GDP by 2030 and would actually mean that there would be a deficit of. 1.2% of GDP by then. The TWG recommended steps were needed to widen the tax base.

Those issues have not gone away and in fact will have been exacerbated because of the increase in borrowings that the Government incurred as a result of the COVID 19 pandemic.

We are not really having a discussion around how are we going to fund an ageing population, the increased demands on health and, as I pointed out last week, adapting to climate change. Every government seems to be stuck around keeping tax limited to 30% of GDP, Bernard Hickey has a long series of very interesting commentary on this.

The Budget documents don’t really address that issue in my mind, and it’s something that, as I’ve said beforehand, we’re going to need a serious discussion around how we expand our tax base and manage these pressures. Superannuation, remember, is now the second single biggest item of Government expenditure. This discussion isn’t going to go away and inevitably it’ll come back to the question of taxation of capital. We probably see the politicians fence around it during next year’s election. But those pressures will remain.

Pressure derails OECD deal?

Now, speaking of politicians under pressure, President Biden had been struggling to get his Inflation Reduction Act through Congress. But this week he managed to do so after a few recalcitrant senators finally came on board.

There’s a couple of interesting implications about this. Firstly, it appears to move forward the possibility of America coming on board with the OECD’s global tax deal. And in particular, the Pillar Two proposal for a minimum corporate tax rate of 15%.

However, it’s emerged that the Biden administration’s changes to the bill in order to get it passed appear to be at odds with how the minimum 15% corporate tax rate % is going to work. The details are a bit complicated, inevitably, but the corporate minimum tax of 15% will apparently only apply to the book income, that is income reported in financial statements of companies with revenue over US $1 billion. It will also only apply on a group level rather than at a country-by-country basis, which is contrary to the intention of the OECD tax deal, of eliminating the practise of setting up subsidiaries in tax havens.

Some international tax experts are saying the Biden deal may not now actually be compliant with the global tax deal. That possibly opens it up for other jurisdictions to say “Hang on, we’re not going to have that”. But ironically, it appears that US multinationals may in fact be keen to get the OECD Pillar Two deal passed through, because otherwise they may be exposed to additional taxes. So, watch this space. The point is, the Inflation Reduction Act is progress even if there are ructions still going on in Europe with Hungary now putting a spanner in the EU’s need for unanimity to agree the deal.

The other quite interesting thing that emerged is that the US Internal Revenue Service, the IRS, got US$80 billion of extra funding. And there’s a story from the Washington Post which explained why it needed that funding.

It includes an absolutely extraordinary photograph of the cafeteria in an IRS office in Austin, Texas. All that is visible is boxes and boxes of paper files, because the IRS had, as of the end of July, a backlog of 10.2 million unprocessed individual returns.

To give you an idea just how archaic the IRS’s system is, paper tax returns aren’t scanned into computers. Instead, IRS employees manually keystroke the numbers from each document into its system, (this is what Inland Revenue previously had to do until its Business Transformation programme).

It is absolutely extraordinary what’s going on with the IRS. I suggest every time you feel that Inland Revenue has dropped the ball and is hopelessly inefficient, thank God you’re not dealing with the IRS. We had a situation where we sent the IRS a letter in January 2020 and we did not get a reply until August 2021, and we were possibly one of the lucky ones.

Giant jump in tax writeoffs

And finally, a little snippet emerged about how much use of money interest the Inland Revenue has written off in relation to the COVID pandemic funding. National MP Andrew Bayly asked the Minister of Revenue how much tax interest and penalties have been written off for the last three financial years. The response was in the year to June 2020, it was $17.8 million, in the year to June 2021, $22.5 million, and in the year to June 2022, $26.8 million. Quite reasonably substantial amounts.

But what was also revealed was how Inland Revenue had applied its increased discretion to write off use of money interest as a result of the COVID 19 pandemic. The total amount remitted between 10th June 2020 and 4th of July 2020 was $104 million, which is way above what I would have ever estimated. This amount probably relates to well over $1 billion of debt, possibly as much as $2 billion. It gives an idea of the fiscal impact COVID 19 has had and will probably continue to have.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

25 Jul, 2022 | The Week in Tax

- Depreciating buildings

- Who are taxed the heaviest?

- The OECD says housing should be taxed

Transcript

Inland Revenue has released Interpretation Statement IS 22/04 on claiming depreciation on buildings. Critical to this issue is determining the meaning of a “building” for depreciation purposes and the distinction between residential and non-residential buildings. The Interpretation Statement addresses this issue when it sets out when depreciation may be claimed for non-residential building and also for some fit outs. It confirms that no depreciation is available for residential buildings.

The Interpretation Statement then sets out where you can find the right depreciation rate for buildings when fit outs attached to buildings may be depreciable. How to treat an improvement of a building for depreciation purposes. And then finally, what happens when the building is disposed of or its use changes?

To recap, depreciation for all buildings was reduced to zero, with effect from the 2011-12 income year. Back in 2020 as part of the initial response to the pandemic, the Government reintroduced depreciation for non-residential buildings with effect from the start of the 2020-21 income year. Generally, the depreciation rate is 2% on a diminishing value basis, or 1.5% on a straight-line basis. Some other depreciation rates may be used where the building has a shorter than normal useful economic life. Examples would be barns, portable buildings or hot houses. Additionally, it’s possible to claim a special rate if the building is used in an unusual way.

Now for depreciation purposes “building’ retains its ordinary meaning which means anything that is structural to the building or used for weatherproofing the building. The Interpretation Statement emphasises that whether a building is residential or non-residential is an all or nothing test. If the building is non-residential depreciation is available, otherwise not, there’s no apportionment.

Residential buildings are any places mainly used as a place of residence. This includes garages or sheds included with that building. Places used as residential residences for independent living in retirement villages and rest homes are residential buildings are is short stay accommodation where there’s less than four separate units.

On the other hand, non-residential buildings include buildings used predominantly for commercial and industrial purposes, but not residential buildings. This also includes hotels, motels, inns, boarding houses, serviced apartments and camping grounds. Retirement villages and rest homes where places are not being used for independent living are non-residential buildings as is short stay accommodation where there are four or more separate units.

If improvements are made to a building, you must treat it as a separate item of depreciable property in the first tax year. Then you can either continue to treat it as a separate item of depreciable property or simply add it to the building by increasing the adjusted taxable value of the building.

In some cases, a fit out can be separately depreciated depending on the nature of the building and the nature of the fit out. Where the fit out is considered structural to the building or used to weatherproof the building it must be treated as part of building and not depreciated separately. Fit outs are depreciable in a wholly non-residential building and sometimes in a mixed-use building. But remember, the key point is that depreciation is not available under any circumstances for a residential building. So overall, this is a useful Interpretation Statement and is also, as has become the norm, accompanied by a very handy fact sheet.

The agencies tackling organised crime and its tax evasion

Moving on, last week I discussed a suggestion by ACT Party leader David Seymour to use Inland Revenue against the gangs. I looked at the powers available to Inland Revenue and discussed how practical his proposal was. To summarise, Inland Revenue has extensive powers which would be useful in tackling gangs and organised crime. However, this is a resource intensive approach which probably in Inland Revenue’s view, would divert its attention from other areas it considers equally important.

This prompted some discussion in the comments section and thank you again to all those who contributed. As I said, my view is Inland Revenue probably thinks other agencies, such as the Police, are better suited for this activity. But it will cooperate with those agencies. Its annual reports make clear they pass information to other agencies. So Inland Revenue is probably working on this matter in the background.

It was interesting just to take a look to see what other agencies were doing in this space and get a gauge of what’s happening. A key tool for the Police is the use of restraining orders to seize assets. According to the Police’s Annual Report for the year ended 30th June 2021 the value of restraints for the year totalled just over $100 million, including nearly $30 million seized from anti-money laundering.

The Department of Internal Affairs also has responsibilities for anti-money laundering, as it’s a key regulator on that. Its Annual Report to June 2021 indicates that perhaps it could do more in this space, as its budget for its regulatory services for the year was set at $52 million, but it only spent $44 million.

And then when you look at the DIA’s performance metrics, such as desk-based reviews of reporting entities, it’s supposed to be targeting between 150 and 350 such reviews annually, but managed only 219 for the year, up from 198 in the previous year. And on-site visits were meant to be somewhere between 70 and 180 but came in at 79. To be fair these were probably disrupted by the impact of COVID 19.

Still, there are other agencies involved in pursuing gangs including Customs who will also be very interested. Inland Revenue will be playing a role, it shares information with these other agencies. So even if it’s not wielding a very big stick publicly, it’s working in the background.

The interaction of tax and abatements on social assistance

Now tax has been in the news a lot recently with the election coming up even though it’s still just over a year away probably. National and the ACT Party have both set out they would proposed some tax cuts. Last Saturday, Max Rashbrooke, a senior associate at the Institute of Governance and Policy Studies, who has written quite a lot on wealth and taxation put out some counter proposals to National and ACT’s proposals.

He suggested that really the focus should be on middle income earners. And he made a suggestion, for example, that we could have a $5,000 income tax free threshold, something we see in other jurisdictions. Britain’s is just over £12,500, Australia’s is A$18,200 and the US has a slightly different thing. It gives you a standard deduction of US$12,000. But anyway, let’s take that comment elsewhere. And Max suggested that something could be done in that space.

But it got me thinking about the question of who does actually pay the highest tax rates in the country. And the answer isn’t those on over $180,000 where the tax rate is 39%, it’s actually more around $50,000 mark if those people are receiving any form of government assistance, such as Working for Families. If they have a student loan as well, then an additional 12% of their salary after tax gets deducted.

The interaction of tax and abatements on social assistance, such as the family tax credit and parental tax credit can mean in some cases, the effective marginal tax rate for some families is more than 100% on every extra dollar they’re earning. This is an issue which the Welfare Expert Advisory Group touched on, but the Tax Working Group wasn’t allowed to address. But it’s a huge problem.

Take, for example, someone earning $50,000, just above the $48,000 threshold where the tax rate goes from 17% to 30%. And that, by the way, is the rate where I think we need to focus our attention on adjustments to thresholds and tax rates. At that level every extra dollar they’re earning is taxed at 30%. If they’ve got a student loan then they pay a further 12%. If they have a young family and are receiving Working for Families tax credits, then these are abated at 27%. Incidentally, the abatement threshold is $42,700. So that means that that person is on a marginal tax rate of 69%. Definitely not nice.

Then there’s a separate credit, the Best Start tax credit which has a separate abatement regime in addition to the Working for Families abatement regime I just explained. So that’s why people could be suffering an effective marginal tax rate of over 100%.

In my view, this is the area where we really need to be thinking about changing the tax system, because to compound matters, governments have been very cynical about not adjusting thresholds for inflation, something I’ve raised repeatedly in the past.

Working for Families thresholds were adjusted for inflation every year until National was elected in 2008. Starting in the 2010 Budget they started freezing thresholds. They also increased the abatement rate which used to be 20% and is now 27%. The current Working for Families abatement threshold is $42,700, which is less than what someone working full time on the minimum wage will earn annually

Looking at student loans the threshold where repayments start in 2009 was $19,084. That is now $21,268 but for a long period of time under the last government it was frozen. National also increased the repayment rate from 10% to 12% in 2013.

So this is an area where governments of both hues have been really quite cynical in my view, and where a lot of serious thought needs to go in about trying to address the inequities that have arisen. The Welfare Expert Advisory Group suggested the abatement rate should be 10% on incomes between $48,000 and $65,000, then increase to 15% before rising to 50% on family incomes over $160,000. (Yes, large families with that level of income could be receiving social assistance in some instances).

There’s a lot of work to be done in this space and inflation adjustments to thresholds is something that should be done anyway. But I think we need to think carefully around the thresholds and how the interaction with social assistance works. At the moment we’re not getting that sort of analysis from either any of the main parties and that’s disappointing, as it’s something that really needs to be addressed.

Why the FER deals with recurrent taxes better

And finally this week, just hot off the press is an OECD report on Housing Taxation in OECD countries. This makes for some interesting reading. Briefly, the report is concerned about how housing wealth is mostly concentrated amongst high income, high-wealth and older households. And in some cases, they believe that a disproportionately large share of owner-occupied housing wealth is held by this group. There’s been unprecedented growth in house prices, not just in New Zealand, but across the whole OECD, making housing market access increasingly difficult for younger generations.

In terms of suggestions the OECD believes that housing taxes are “of growing importance given the pressure on governments to raise revenues, improve the functioning of housing markets and combat inequality.” The report notes the way housing taxes are designed often reduces their efficiency. Recurrent property taxes, such as rates, are often levied on outdated property values, which significantly reduces their revenue potential. This also reduces how equitable they are because where housing prices have rocketed up, people are underpaying based on current values. And conversely people in places where prices are falling or have been stagnant are paying more relative to those in richer areas.

One of the suggestions the report makes is that the role of recurrent taxes on immovable property should be strengthened, by ensuring that they are levied on regularly updated property values. And this is one of these reasons why Professor Susan St John and I have been promoting the Fair Economic Return approach. One of the strongpoints of our proposal would be strengthening the role of recurrent taxes.

Capping a capital gains tax exemption on the sale of a primary residence

Another proposal would not at all popular. It is to consider capping the capital gains tax exemption on the sale of main houses so that the highest value gains are taxed. This should strengthen progressivity in the system and reduce some of the upward pressures. This is what happens the U.S. There is a US$250,000 exemption on the main home per person, and above that the gains are taxed. There’s no reason why we shouldn’t have a similar type exemption here if we want to introduce a capital gains tax. But as I said, that would be particularly unpopular.

The OECD also believes there should be better targeted incentives for energy efficient housing, because housing, according to this report has a significant carbon footprint, maybe 22% of global final energy consumption and 17% of energy related CO2 emissions.

So, there’s a lot to consider in this report, and we come back to it and consider it in more detail. But again, it sort of comes to this point we’ve talked about repeatedly on the podcast, the question of broadening the tax base and the taxation of capital. These issues aren’t going to go away, particularly when you consider, as I mentioned a few minutes ago, how very high effective marginal tax rates are paid by people on modest incomes who may not have any housing. No doubt we’ll be discussing all these issues sometime again in the future.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

18 Jul, 2022 | The Week in Tax

- Using tax law against gangs

- OECD tax coordination on MNCs

- Ireland’s tax risks

Transcript

Last Saturday, the ACT party leader David Seymour appeared on Newshub Nation and suggested that Inland Revenue be used to deal with the gangs.

He believed the powers currently being used by Inland Revenue as part of its high wealth individual research project could equally be applied to deal with the gangs. It did make for some entertaining viewing, as interviewer Rebecca Wright was more than a little incredulous at the suggestion that gang members wearing patches would happily submit to filling out questionnaires. On the other hand, the notorious mobster Al Capone, was ultimately jailed for tax evasion so the use of Inland Revenue against organised crime is not that unreasonable a suggestion.

Mr. Seymour does seem to have misunderstood the nature of the powers currently being used by Inland Revenue as part of its high wealth individual research project. Those powers have been deliberately limited so that the information gathered is solely for research purchase purposes. They are therefore more prescribed than the general powers available to Inland Revenue. I also think Mr. Seymour was overstating how much of a sanction non-compliance with the high worth individual research project would be.

Now Inland Revenue does indeed have some extensive powers of information request and where appropriate, search and seizure. And if you want an example of how it can apply those rules that can be found in the case of Tauber v Commissioner Inland Revenue.

In this case, Inland Revenue was investigating a former accountant who it believed was suppressing income. After its initial information requests were not satisfactorily answered in its view, Inland Revenue then decided to use the powers available to it under Section 16 of the Tax Administration Act. It carried out simultaneous search and seizure operations at six separate locations, including a boat shed.

Mr Tauber responded by making an application for judicial review, claiming that the various Section 16 warrants were too widely drawn and not specific enough. The application also questioned whether the searches were necessary for carrying out the Commissioner’s functions and if the searches were carried out in an unreasonable manner. Unfortunately for Mr Tauber and the other claimants the courts upheld Inland Revenue’s use of its powers.

The case illustrates the extensive powers available to Inland Revenue. However, what it also illustrates is that applying those powers is a very intensive operation requiring a considerable number of resources. If you’re raiding six properties simultaneously with teams of investigators, you’re talking about an operation which may have involved somewhere between 40 and 50 people. Now if you think about dealing with gang members Inland Revenue would also want to be raiding several premises simultaneously. Therefore, that would require considerable resources from it and no doubt police officers to be available in case matters escalated.

It’s therefore questionable whether Inland Revenue would actually have the resources to carry out major investigations into gangs. And although tax evasion is a criminal offence, Inland Revenue would probably be of the view that the powers available to police and other authorities under the anti-money laundering legislation, which have been strengthened this week, mean those agencies are more appropriately deployed to deal with organised crime.

This isn’t to say that Inland Revenue wouldn’t pass up the opportunity to investigate tax evasion involving gangs if it felt considerable sums were involved. But as the Tauber case shows, using its full range of investigatory powers requires considerable resources, which ultimately, I think, Inland Revenue might feel better used elsewhere. In other words, “Nice idea, but yeah nah.”

Update on OECD tax reform

Moving on, the OECD delivered its latest update on the status of the international tax reform agreement to G20 finance ministers and central bank governors a couple of weeks ago. This included a progress report on the status of Pillar One, which is the proposal to ensure that market jurisdictions can tax profits from some of the largest multinational enterprises.

The OECD Secretary-General presented a comprehensive draft of what these proposed technical model rules will be for Pillar One. These are now going to go out for public consultation between now and mid-August. The intention then is to finalise a new Multilateral Convention by mid-2023 for entry into force in 2024.

In addition to updating the status of the Multilateral Convention to implement Pillar One, the Secretary-General’s Tax Report also gave an update on how an implementation of the OECD transparency agenda (the Common Reporting Standards on The Automatic Exchange of Information). And the latest update is that information on at least 111 million financial accounts worldwide covering total assets of nearly €11 trillion was exchanged automatically between tax administrations in 2021. And later this year, the OECD will finalise a new crypto-assets reporting framework, which will be included as part of the Common Reporting Standards. So things are moving ahead even if they’re going more slowly than people had expected.

In relation to the Pillar Two work, which introduces a 15% global minimum global minimum corporate tax rate, the technical work on that is largely complete and an implementation framework is to be released later this year to facilitate the implementation and coordination between tax administrations and taxpayers. All G7 countries, the European Union and several other G20 countries, along with several other economies, have scheduled plans to introduce the global minimum tax rules. New Zealand hasn’t reached that stage but consultation on the matter has just ended, so we may see something later this year.

IRELAND’S TAX RISKS

Now one of the ideas behind the Pillar Two global minimum corporate tax rate is to try and stop tax competition driving corporate tax rates lower. Now, one of the poster child’s for lower corporate tax rates is Ireland. And last week I mentioned Ireland’s strong GDP per capita growth in recent years. This appears in part to be a by-product of multinational and multinational investment in Ireland, attracted by Ireland’s low corporate tax rate of 12.5%.

Now tax is always full of unintended consequences and this week the Irish Finance Ministry highlighted a potentially huge downside of this policy for Ireland.

Apparently just ten multinational firms pay over half of Ireland’s corporate tax receipts. These are expected to be between €18 and €19 billion this year, up from an estimated €16.9 billion forecast just three months ago. And by the way, that’s nearly a five-fold increase in the last decade.

Now, on the face of it that all sounds good. But John McCarthy, the Irish finance ministry’s economist, warned that the fact that just ten multinational firms pay more than half of honest corporate tax, represents “an incredible level of vulnerability” for the Irish economy, as a shock, which impacted on the multinational sector would have severe fiscal implications for Ireland. I understand something like one in nine Irish employees are employed by multinationals such as Facebook, Google and Pfizer. Therefore, the fallout from a shock in this sector could be huge for Ireland.

Mr. McCarthy told reporters the level of concentration in such a small number of firms is something he has never seen in any other economy. He was therefore more worried about the overreliance on these types of firms than the impact of the global overhaul of corporate tax regimes could have on Ireland’s position as a hub for multinational investment. Ireland power. The same report estimates that Ireland’s tax take would be affected negatively by about €2 billion over the medium term.

Irish Finance Minister Paschal Donohoe then chipped in saying he has long shared the concerns McCarthy outlined. He said the best way to manage the risk was to return to the pre-pandemic position where corporate tax receipts are not used to fund permanent spending. This seems an incredible admission that a low corporate tax rate is actually not sustainable over the long term. So that’s something to pause to think about when you hear talk about corporate tax cuts.

By the way, these concerns of the Irish finance minister and the Finance Ministry might explain why Ireland didn’t oppose the proposed 15% global minimum tax rate. I suspect that on the quiet this represents an opportunity for Ireland to raise its corporate tax rate without too much fuss. It would be interesting to know the level of concentration here in New Zealand. I guess the big four Australian banks and the New Zealand Superannuation Fund would represent at least 20% of the corporate income tax take.

IRD BACK LIQUIDATING DEFAULTERS

Moving on, a quick follow up from last week’s items about Inland Revenue’s enforcement and collection activity increasing. As of 30th June 2021, 140,000 taxpayers had arrangements with Inland Revenue covering $3.7 billion of tax. Now, Inland Revenue would be keen to ensure those numbers don’t continue to grow. Historically, what it’s done is taken strong enforcement action including initiating liquidations. Apparently about 70% of all high court liquidations were initiated by Inland Revenue. However, during the pandemic, as part of its more sympathetic response, that number fell to just under 30%.

However, I’ve been informed that since April that there’s been a huge escalation in Inland Revenue activity in the High Court and liquidation proceedings. So that’s the clearest sign of Inland Revenue’s increased focus on debt collection and a clear warning to all those out there that if you if you’re in trouble you need to front up and try and make arrangements with the Inland Revenue before they take it further to the liquidator.

AWARDS FINALISTS

And finally, this week, the Tax Policy Charitable Trust has just announced its four finalists in this year’s Tax Policy Scholarship competition.

This competition is designed to support tax policy, research and thinking. Entrance is limited to those under the age of 35, and the intention is that people are asked to give ideas of proposals for reforms to our current tax system, to address potential weaknesses and unintended consequences of existing laws. Now there are three topics in this year’s competition: environmental taxation, tax, administration generally, or the powers granted to the Commissioner of Inland Revenue and to investigate for research policy purposes. (These are the powers that Mr. Seymour was referring to in his interview about tackling the gangs).

The four finalists are Daniel Doughty, a senior consultant with EY in Wellington. He’s proposing a small business consolidated reporting regime to simplify tax reporting for small companies. I think this is an excellent suggestion, so look forward to finding more about this. Our tax system expects a lot of administration from small businesses without really trying to adjust the compliance burden to help them with those processes.

The second finalist is Mitchell Fraser, a tax solicitor with Mayne Wetherell in Auckland. Mitchell is worried that the new powers granted to Inland Revenue for tax policy purposes may have unintended consequences. He’s suggesting alternative means to collect the information that’s wanted, including through Statistics New Zealand.

The third finalist is Vivien Lei, a group tax advisor with Fisher Paykel Healthcare. Vivien has got another interesting proposal to change New Zealand’s environmental practises by introducing an impact weighted tax regime. Under this model, organisations will be taxed on a net positive or negative impact on the environment. Now this is an area I’m very interested in and previous readers or listeners of the podcast will know that John Lohrentz, one of the runners up in the last competition, proposed a progressive tax on bio genetic biogenic and methane emissions in the agriculture sector. It’s therefore good to see there’s plenty of focus on this area.

And finally, there’s Jordan Yates, a senior tax consultant with ASB in Auckland, and he believes the tax policy landscape has been fractured and suffocated by political roadblocks. I don’t think he’s wrong there. Jordan’s proposing an independent statutory authority that would be responsible for the independent management of fiscal policy as it relates to the tax base. It’s an idea I’ve heard floated in other places and another one I look forward to hearing more about. This fracture is one reason why the Minister of Revenue, David Parker, has proposed his Tax Principles Act.

The finalists have all been asked to develop a 5,000-word submission on their proposal. They’ll then make a final presentation and answer questions at a function later this year in October, after which the winner will be announced.

This is a great initiative by the Tax Policy, Charitable Trust, and I look forward to hearing more about these proposals. And as we did with Nigel Jemson, the winner of the last competition and runner-up John Lohrentz we will hopefully have the prize winners on the podcast.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

30 May, 2022 | The Week in Tax, Uncategorized

- Will the IRD be able to deliver the cost-of-living payment?

- Potentially unwelcome GST surprise for farmers selling up.

- The latest developments from the OECD

Transcript

In the wake of the Budget, a Cost of Living Payments bill was introduced and has now been enacted. As part of the enactment a supplementary analysis report was released giving background to the proposed $350 payment. And this supplementary analysis has some very interesting commentary.

It appears the Cost of Living Payment was put together very much at the last minute as a response to the adverse effects of inflation on low to middle income households. According to these documents, this report was finalised on May 4th, barely two weeks before the Budget was delivered, which is very late in budget terms.

According to the document, Inland Revenue recommended against being the delivery agency for this Cost of Living Payment. The reason it gave was that it was concerned, that being asked to administer the payment would significantly impact its services to customers – taxpayers in plain English.

“The addition of this payment to their portfolio of services Inland Revenue already delivers will compromise Inland Revenue’s already stretched workforce and affect the taxpayer population, including the families and individuals that the payment would be intended to support them.”

Inland Revenue correctly identified that as soon as the announcement was made, they would get contacted about it which would put strains on their systems. It calculated a maximum of approximately 750 full time equivalent staff would be required to handle the payments to be made in the weeks of 1st August, 1st September and 1st October. Now, to put that in context, Inland Revenue staff as of 30th June 2021 was 4,200 full time equivalents. It would therefore need to use the equivalent of 18% of its staff to handle the delivery of this Cost of Living Payment. Quite clearly this would put strains on its system. The $816 million appropriation for the Cost of Living Payments includes $16 million to Inland Revenue for delivery of the services.

It’s therefore likely that Inland Revenue will need to hire additional staff, presumably contractors, on a short-term basis. And as we’ve discussed previously, the issue of contractors hit the courts with the Employment Court ruling that the contractors were not employed by Inland Revenue although I understand that decision is being appealed.

It also seems the Inland Revenue poured a bit of cold water on how the payments would be structured. According to the report, 55% of the total payments to be made will be to the middle 40% of households, 20% would be made to the bottom 30%, and 25% would go to the top 30%. There would be an estimated 478,000 households with children and 610,000 households without children who would receive a Cost of Living Payment. Although around 60% of all potentially eligible recipients will have annual income below $70,000, 10% would have family income of between $70 and $100,000 and 30% will have family incomes over $100,000.

And this led Inland Revenue to point out that potential equity concerns could arise because using individual income to calculate the eligibility for the payment rather than household income may result in different outcomes for households with the same income level. For example, a single person earning $100,000 won’t receive a payment, but a household with two people working who each have income of $50,000 would both receive the payments.

There’s also some analysis regarding how the eligibility is dependent on a person’s prior year’s income, which means the tax returns for the March 2022 must be filed. The paper notes that by the time Inland Revenue begins making payments on 1st August, it expects to have already raised individual tax assessments for approximately 3.2 million individuals, about 75% of individual taxpayers. But that leaves about 500,000 individuals, who may not initially receive the payment between the August to October payment run period because they haven’t filed their tax return. And this includes people who file through tax agents and have in theory until 31st March 2023 to file last year’s tax return.

This underlines a point I made in last week’s Budget commentary that you can probably expect tax agents to come under more pressure to get tax returns done on time so that those people who think they’re eligible may get a Cost of Living Payment. Overall, it’s some interesting insights into the administration of these systems and the Budget process.

GST pitfalls for the unwary

Now moving on, GST is probably the best example you can find of the broad-base low-rate approach to taxation policy. But even though it’s a highly comprehensive tax, that does not make it a simple tax. In fact, it’s full of pitfalls for the unwary. And I’ve been alerted to one which may affect farmers who are selling up.

Back in 2020, Inland Revenue caused some consternation when it issued Interpretation Statement IS20/05 on the supplies of residences and other real property. The Interpretation Statement reversed a long-established policy since 1996 on the sale of the farmhouse where the farmer might have used part of the property for their taxable activity, for example a home office in the homestead. Previously Inland Revenue’s position was that the sale of a farmhouse would generally be a supply of a private or exempt asset and not subject to GST.

However, in IS 20/05, Inland Revenue reversed that position and now said that the sale of the dwelling would have been useful for families who would now be subject to GST. The example the Interpretation Statement gave was if a GST registered farmer was claiming an automatic 20% deduction for farmhouse expenses, an Inland Revenue would expect that the property was therefore being used 20% of the time in the taxable activity and consequently sale of the farmhouse would be a supply in the course or furtherance of a taxable activity and therefore subject to GST.

This change has caused some consternation although some relief was given in the recently enacted Taxation Annual Rates for 2021-2022, GST, and Remedial Matters Act. This included a provision which allowed a deduction for the private use portion of a sale. Coming back to that 20% example I mentioned a moment ago, if 20% of the homestead was used for farming business and 80% for private purposes, there would be an adjustment for the output tax of 80% of the private portion. But that would still mean that 20% of the current value of the farmhouse at the time of sale would be subject to GST, which would be an increased tax burden for many farmers and undoubtedly a surprise for some.

Apparently Inland Revenue is now indicating that it may reconsider its position in its Interpretation Statement, which is a classic example of the military maxim “Order, counter-order, disorder”. But until that point is clarified, farmers who are selling their farm should be aware of this potential liability and seek advice on that transaction.

How the OECD influences our tax policy

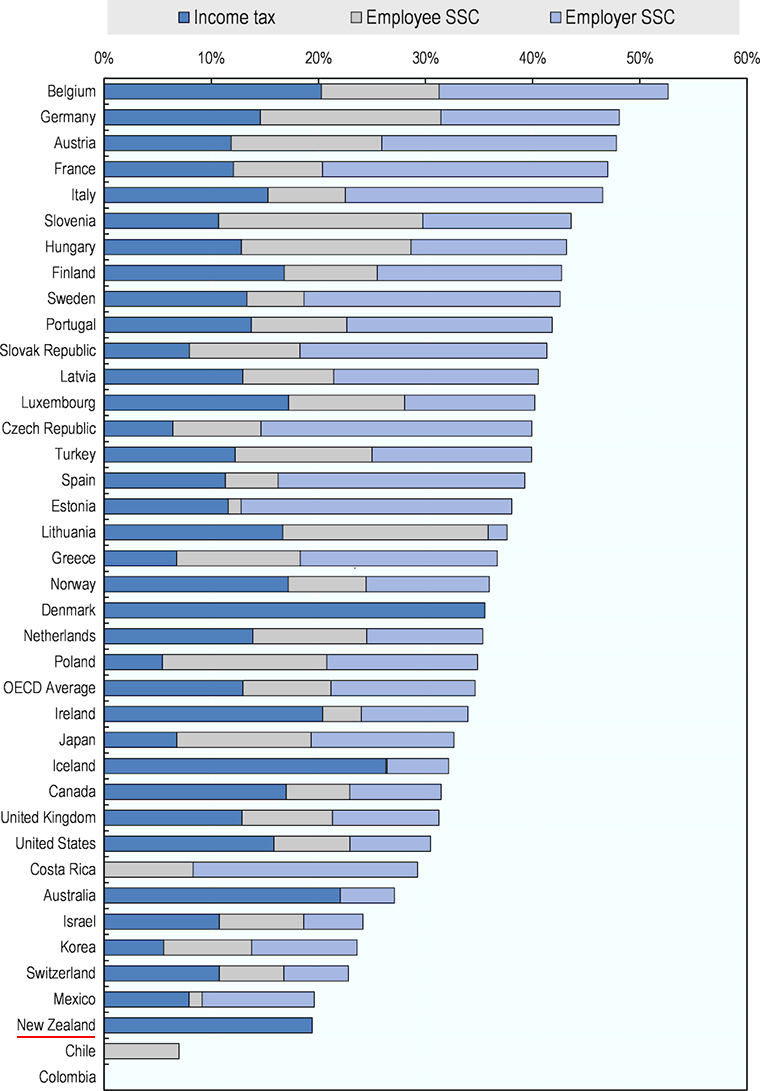

And finally this week, a couple of updates from the OECD. Firstly, it released its annual report on the taxation of wages. This includes its tax wedge analysis, which looks at the difference between labour costs to the employer and the corresponding net take home pay for the employee. Basically, the tax wedge is the sum of the personal tax income tax payable by the employee plus any employee and employer social security contributions plus any payroll taxes less any benefits received by an employee. (I think ACC is included for these purposes).

As can be seen New Zealand, scores very highly with a tax wedge of 19.4%, which is the third lowest in the OECD. The average in the OECD is 34.6%.

What this tax wedge measure also points to is the significance of Social Security and payroll taxes in other jurisdictions. One of the criticisms of the Government’s proposed social insurance scheme is it would be the first real Social Security tax that New Zealand has. It seems from early feedback this is one reason employers are pretty reluctant about the scheme. But even if the scheme was introduced, we’d still be down the lower end of the tax wedge.

Now the second OECD report was titled Tax Cooperation for the 21st Century. This was prepared by the OECD for the G7 finance ministers and central bank governors when they met recently in Germany. It’s particularly interesting because it picks up on what’s been happening with the adoption of the Two Pillar solution for international taxation we’ve talked about recently.

The OECD was asked to prepare was a report that would focus on the further strengthening of international tax co-operation and what recommendations it has in this field. This is looking beyond the implementation of the Two Pillar solution which makes it very significant, in my view, about the future administration of international tax.

For example, a key recommendation is tax administration should be seen as a common mission by tax authorities rather than a potentially adversarial exercise. The development of international cooperation is one of the biggest themes in international taxation in the 21st Century and is also probably one of the least understood. And I will repeat what I’ve said beforehand, most people are oblivious to the amount of information that is being shared by tax authorities at all levels. China, incidentally, has just signed up to the mutual agreement and protocols on that. So every major jurisdiction in the world is cooperating or looking to cooperate on international tax at some level. This is why this paper is important because it starts to map out and where that international co-operation might be going.

The report focuses initially on corporate tax saying there needs to be a reliable framework for cross-border investment. As just noted, tax administration should be seen as a common mission. There should be a collaborative approach with early and binding resolution.

The impact of going digital is emphasised and that it needs to speed up to improve engagement with taxpayers. There are also recommendations beyond corporate tax about moving to real time data availability for taxpayers and tax administrations to make efficient use of evolving technologies while maintaining data privacy and confidentiality.

The issue of data privacy and confidentiality is a developing area where taxpayers are starting to push back against tax authorities because they are concerned, rightly, whether everything is secure as it should be. Furthermore, some are, understandably, not too happy about information sharing.

Finally there’s a recommendation that advanced economies should commit to supporting developing economies so that they can fully benefit from the policy changes. This means building capacity which is going to be needed, especially for the implementation of the Two Pillar solution. Overall, this is a relatively brief but fascinating paper with potentially significant implications.

And just incidentally, on the international Two Pillar solution, the Secretary General of the OECD has now indicated that he expects that implementation will be delayed by a year until 2024. That doesn’t surprise me, given the scale of the project, because there’s a lot of legislation that needs to be put in place by the middle of next year at the latest. Inland Revenue have only just started consultation on the matter.

Still, the Two Pillar project has moved on quicker than some cynics might have expected. But as I’ve said previously, politics is likely to get in the way, particularly the upcoming US Congressional midterm elections. Anyway, as always, we shall bring you the news as it develops.

Well, that’s all for this week I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

11 Apr, 2022 | The Week in Tax

- Comparing New Zealand’s taxation of property with other countries

- OECD heralds a clampdown on crypto assets

- Another warning from Inland Revenue about attempts to manipulate income to avoid the 39% tax rate

Transcript

In last week’s Sunday Star Times, Miriam Bell looked at the question of how New Zealand’s taxation of property compares with other jurisdictions.

In doing so, she spoke to myself, Robyn Walker of Deloitte, and John Cuthbertson, the tax director for Chartered Accountants Australia and New Zealand. We all gave differing takes on the position.

According to the OECD statistics, we are near the bottom end of the range as a percentage of GDP. Including local government rates, New Zealand’s taxes on property for 2020 was approximately 1.9% of GDP and the total tax take for the year of 32.18% of GDP. By comparison, Australia’s taxes on property was 2.718% of GDP (2019 numbers), the UK was 3.855% and Canada 4.15% of GDP (both 2020 numbers).

As you can see, Canada and the UK are significantly above New Zealand. One of the reasons for this, as Robyn and John pointed out, is that they have a range of stamp duties that may apply. But also, as we all pointed out, all three jurisdictions, Australia, Canada and the UK, also have capital gains tax and in the case of the UK, inheritance tax may also apply on some properties on transfer.

The article provoked a fairly lively debate, as you would expect. The range of views across the board is that, yes, it looks like we’re under taxed. But the bright-line test is in place which is problematic in that although it looks like a capital gains tax, it doesn’t apply comprehensively, unlike in the other three jurisdictions.

Robyn Walker then made a very good point following through that the design of the bright-line test is basically all or nothing. If you hold property for more than 10 years, you’re outside the test, which means that you’re likely not to be taxed on it. So you get this wide variance in the tax effect of sales or property, which you don’t see to the same extent in other jurisdictions.

Robyn subsequently did a nice little post on LinkedIn, in which she looked at what would be the tax consequences in Australia, Canada, the UK, and New Zealand for the sale of a property which realised a $100,000 gain. Because we treat it as income, we’ll tax the full gain at the relevant marginal rate and for the purpose of the example that was 33%. Canada and Australia will tax only half the gain at the relevant marginal rate, although non-residents in Australia will be taxed on the full gain. And although the UK will tax the full gain the top rate applicable is 28%.

The end result was that if the bright-line test applied, then the tax payable in New Zealand would be highest relative to the other three jurisdictions. But if the bright-line test didn’t apply, then it was the lowest. In fact, it would be nil. And this reinforces Robyn’s point that it is a poorly designed test which can be very unfair in its application. You hold a property for nine years and 363 days, you’re taxed. Hold it for 10 years and one day you’re probably not.

The point I stressed in the article is that we want to look at broadening the range of taxation, and it’s fair if we do so because we start to get round these arbitrary distinctions. As I’ve previously said, my preferred methodology for expanding the taxation of capital is that promoted by Associate Professor Susan St John and myself the fair economic return, not a transactional based capital gains tax.

Anyway, this debate will continue to run and run. Miriam Bell’s article provoked a fierce reaction on Stuff, unsurprisingly, and there’s been an interesting debate around Robyn’s LinkedIn article. I urge you to take a look at that.

I think we really do need to address the issue of taxing property particularly when you consider what the Infrastructure Commission said earlier this week about property owners benefiting to the extent of house prices being 69% higher than they would have been without actions being taken to restrict the supply of housing. Housing and the taxation of property is a touchpoint now and will be in next year’s election. We’re going to see plenty more of this debate

Taxes on crypto assets are coming

Moving on to another controversial asset class – crypto assets. Now the value of crypto assets has just simply exploded in the last 10 years. Because of the explosion of the value, it has forced its way onto the tax agenda and tax authorities all around the world are looking to see how this new asset class fits in with their existing rules. New Zealand is no different from other jurisdictions which are all struggling with this. The recent tax bill that was passed last week, by the way, had provisions relating to the application of GST on crypto-assets.

A couple of weeks back, the OECD released a public consultation document proposing a new tax transparency framework for crypto assets. What it has identified is that crypto assets can be transferred and held without going through the normal financial intermediaries, such as banks, and fund managers. And from a tax perspective, there’s no central administrator having what the OECD calls full visibility on either the transactions carried out or on the location of crypto asset holdings.

It also appears that malware attacks and ransomware attacks, payments are increasingly demanded in crypto-assets, which are largely untraceable. So that’s obviously a matter of concern to not just tax authorities.

The OECD paper also points out that some new paid payment products. Such as digital money products and central bank digital currencies, which also provide electronically storage and payment functions similar to money held in traditional bank accounts.

But at the moment, none of these are covered by the Common Reporting Standard on the Automatic Exchange of Information. A reminder the Common Reporting Standard is an agreement between almost 100 jurisdictions where they agree to swap information on financial accounts held in their country by citizens or tax residents of another jurisdiction. It’s been a huge step forward in tackling adn improving tax transparency and tackling tax evasion.

And what the OECD is proposing is, it wants to develop a new global tax transparency framework, which will involve the same reporting for transactions related to crypto assets as for financial assets covered by the Common Reporting Standard. And it’s calling this the Crypto Asset Reporting Framework, or CARF. The paper proposes that the following types of transactions involving crypto assets will be reportable under the CARF:

- exchanges between crypto assets and fiat currencies;

- exchanges between one or more forms of crypto assets;

- reportable retail payment transactions; and

- transfers of crypto assets.

This would bring about a very significant change in the crypto asset world as a result. It will basically be bringing the whole crypto asset world in line with other reportable transactions under the existing Common Reporting Standard framework. I doubt that will be very popular with investors in the crypto world, but it certainly will be for tax authorities and other authorities, such as financial regulators and police, as they deal with the implications of the arrival of this asset class. Consultation is now open on the document through until 29th April.

Same old problem returns

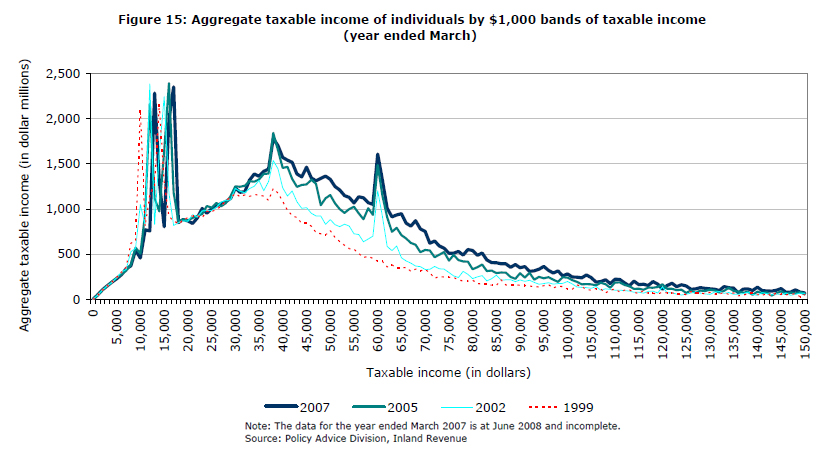

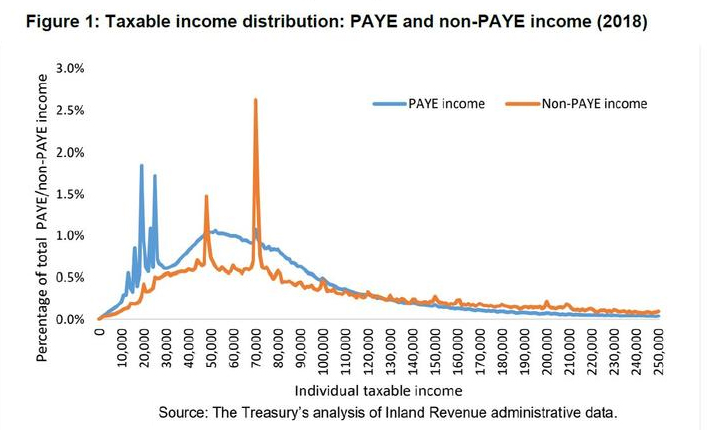

And finally, this week, a couple of weeks ago I discussed the new Inland Revenue consultation paper on countering attempted top tax rate avoidance. It so happens that yesterday RNZ had a story on the paper and Inland Revenue’s concerns that “structures may be being used to reduce incomes below $180,000.”

Inland Revenue has provisionally estimated that income from these high earners will be down $2.88 billion, or about 14% from the year prior. This is on the basis that the average self-employed person – who has the most control over their income – might declare 13% less income than they did the year before, to drop from $191,000 to $166,000 (and by happy coincidence below the $180,000 threshold). The number of PAYE earners is expected to reduce, and also declare lower incomes, from an average of $228,000 to $217,000.

If that is happening then I would expect Inland Revenue to react aggressively. On the other hand, Inland Revenue has known for some time that self-employed income spikes around the $48,000 mark (the threshold when the tax rate increases from 17.5% to 30% and $70,000 dollars when the threshold tax rate increases to 33%). I’m not yet aware of increased Inland Revenue investigation activity into such apparent income manipulation. It seems to me that although Inland Revenue has concerns about manipulation involving the new 39% tax rate, what appears to be happening around the $48,000 and $70,000 thresholds seems very blatant.

The RNZ report included a chart from Inland Revenue of the taxable income distribution for the 2018 income year which illustrated these spikes occurring at the $48,000 and $70,000 thresholds.

The graph mirrors one produced in 2008 (when the top tax rate was 39%). You can see exactly the same pattern of income spikes around $38,000, the threshold at which the tax rate increased from 19.5% to 33% and then at $60,000 when the tax rate rose from 33% to 39%.

In other words this is a very longstanding problem and the question arises why that issue has been allowed to continue? Does Inland Revenue have the resources to address it? They most certainly will say they do, and they would also probably say that they have had a lot to deal with managing the COVID-19 response over the last two together with finalising the Business Transformation project. Either way you should expect action on this from Inland Revenue.

Incidentally on the question of high tax rates, another news report covered the effect of increases for working for families tax credits. It pointed out that the effective marginal tax rate for recipients of working for families can in some cases be 57%. This is the combination of 30% tax rate on incomes over $48,000 and the 27 cents in the dollar abatement, which applies above a threshold of $42,700.

So before people start complaining about 39% being a very high tax rate, think about what’s going on with working for families, accommodation supplement and other social welfare payments. It’s quite conceivable that someone on $60,000 per annum, receiving working for families with a student loan could have a marginal tax rate on every dollar earned of 69%. This represents 30% income tax, 27 cents on the dollar abatement on their working for families and 12% student loan repayments.

By the way, the $42,700 threshold when the working for families’ abatement kicks in is now, by my calculations, less than the annual income of someone working 40 hours a week on the current minimum wage would earn. It’s another case of where governments have allowed inflation to quietly increase the tax take with worse consequences for people at the lower end of the scale. Yet another issue we’ve talked about repeatedly.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time, kia kaha, stay strong.